As a regular user and proponent of Wealthsimple for its investing products and prepaid cash card, I was excited to recently receive an invitation to join the beta for the new Wealthsimple Visa Infinite credit card. Shortly thereafter, I was further invited to upgrade my card to the Wealthsimple Visa Infinite Privilege credit card, essentially the exact same product but with a few added benefits and features.

In this article, I break down the details of these two new entrants to the Canadian credit card market to help you decide if and where they might fit in your wallet.

Overview

| Wealthsimple Visa Infinite | Wealthsimple Visa Infinite Privilege | |

|---|---|---|

| Annual Fee | $240 (billed at $20/month, waived for Premium/Generation clients or with $4,000+ in monthly direct deposits) | $240 (billed at $20/month, waived for Premium/Generation clients or with $4,000+ in monthly direct deposits) |

| Supplementary Cardholders | Not available | Not available |

| Minimum Income Requirement | $60,000 personal or $100,000 household or $250,000 in assets with Wealthsimple | $150,000 personal or $200,000 household or $400,000 in assets with Wealthsimple |

| Card Material | Metal ONLY if Premium or Generation client | Metal ONLY if Premium or Generation client |

| Airport Lounge Access | No complimentary lounge access. | 6 Airport Lounge Passes Per Membership Year (Via Visa Airport Companion Program) |

(No) Welcome Bonus

Neither the Wealthsimple Visa Infinite Card nor the Wealthsimple Visa Infinite Privilege Card offers a traditional “points-based” welcome bonus currently. This is a shame, as most cash back cards in the market do come with at least some sort of temporary boost in earn rate or a statement credit tied to increased spending.

| Credit Card | ||

|---|---|---|

|

None Estimated value: $0 |

|

|

None Estimated value: $0 |

|

Since the card is still in a limited rollout period, it’s entirely possible this will change in the future. When it comes to other products like their investing platform, new customer bonuses are frequent and generous, so I wouldn’t be surprised to see a bonus offered on these cards in the future.

Income & Asset Requirements

The Wealthsimple Visa Infinite requires one of the following:

- Personal Income: $60,000+

- Household Income: $100,000+

- Assets with Wealthsimple: $250,000+

These are standard income requirements for Visa Infinite level credit cards in Canada.

The Wealthsimple Visa Infinite Privilege requires one of the following:

- Personal Income: $150,000+

- Household Income: $200,000+

- Assets with Wealthsimple: $400,000+

These are standard income requirements for Visa Infinite Privilege level credit cards in Canada.

Earning Rates: 2% on Everything

The Wealthsimple Visa Infinite and Privilege cards earn cash back for all eligible purchases at the following rates:

- 2% Cash Back on ALL eligible purchases

There are no categories or spending limits tied to this 2% rate, whether you spend $1,000 or $100,000 in a year. This is the main advantage of the card, particularly for heavy spenders or those who want to keep things simple without micro-managing 3-5% bonus categories.

And unlike competitors that offer 4-5% on groceries but 1% on everything else, this card wins if your spending is heavy on “non-category” items like tuition, Costco, medical bills, or general retail.

Read More: Best Cash Back Credit Cards in Canada

If you aren’t able to waive the annual fee (detailed below), then your required spending to break even on the annual fee each month would be $1,000, earning $20 cash back to offset the $20 monthly fee.

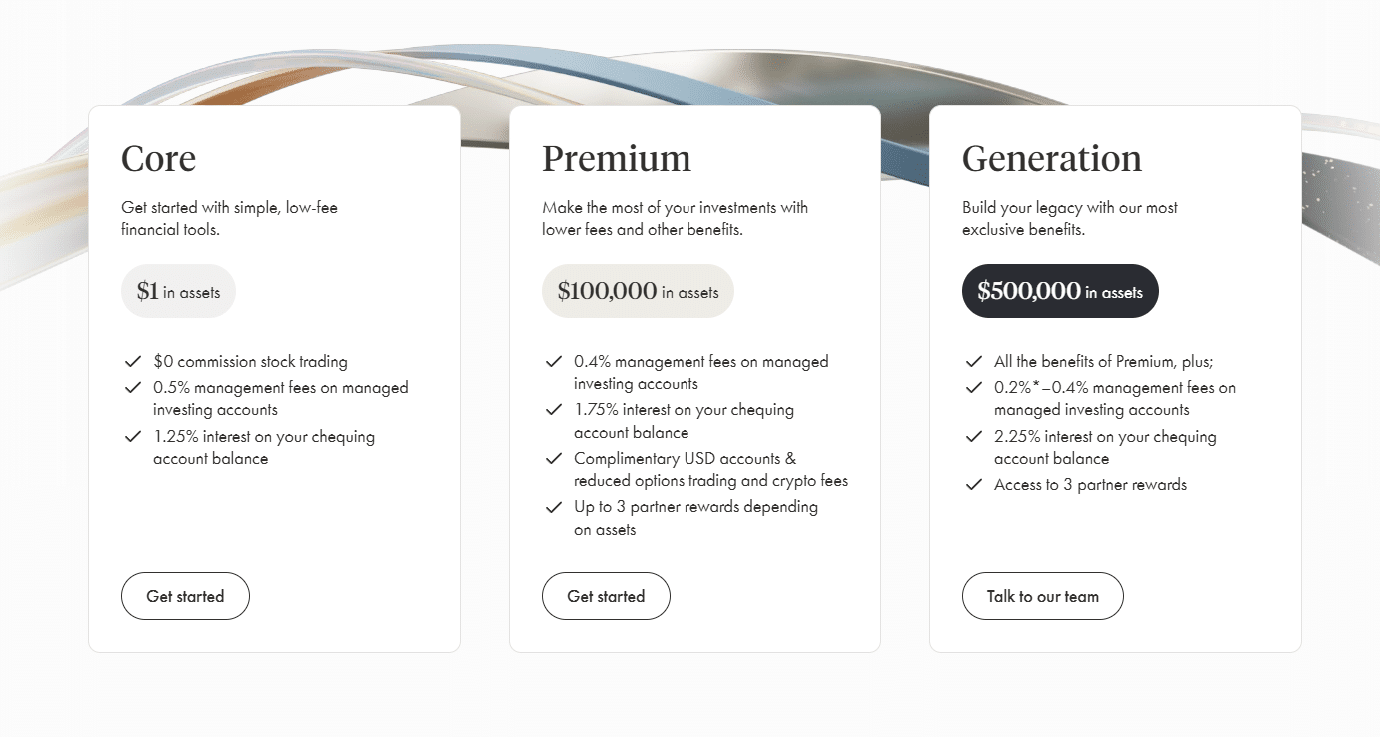

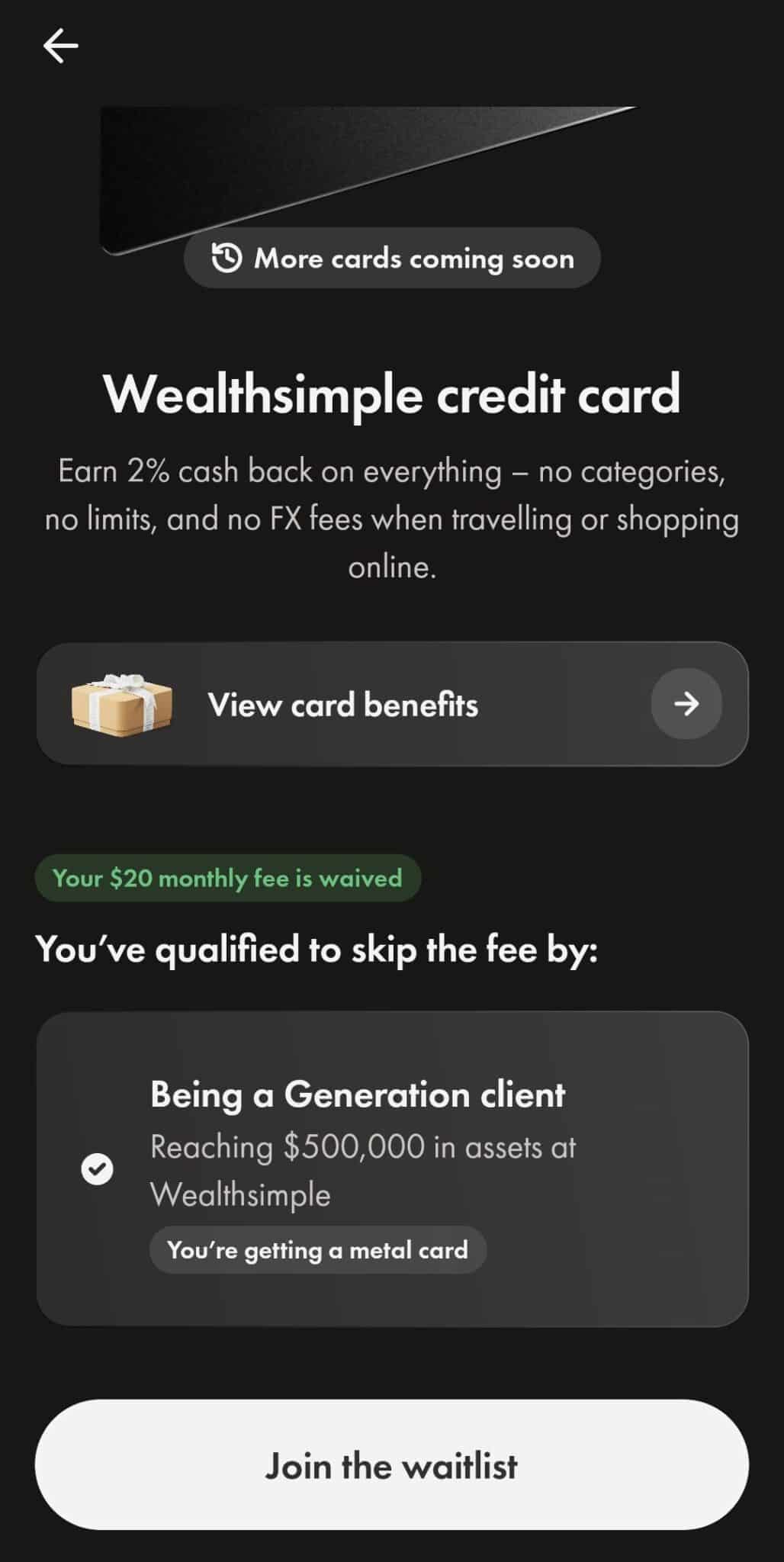

Annual Fee: The “Ecosystem” Waiver

The Wealthsimple Visa Infinite card and the Wealthsimple Visa Infinite Privilege have a monthly fee of $20 (amounting to $240 per year).

How to Get the Fee Waived: You pay $0 if you meet one of these criteria:

- Status: You are a Premium ($100k+ assets) or Generation ($500k+ assets) client.

- Direct Deposit: You deposit at least $4,000/month into your Wealthsimple Cash account.

Qualifying direct deposits include payroll, CPP, Old Age Security, and Employment Insurance. This requirement for direct deposit is intended to encourage customers to hold a greater portion of their cash and assets within the Wealthsimple ecosystem.

Along with the annual fee waiver, Premium and Generation tiers come with a host of other benefits across Wealthsimple products.

Benefits

No Foreign Exchange Fees

There is a dwindling number of credit cards in Canada that come with no foreign transaction fees. The Wealthsimple cards jump onto that list with their 0% fee on foreign currency purchases.

The savings on standard 2.5% FX fees can add up quickly. On a $2,000 vacation spend, this saves you $50 instantly, and this is on top of the 2% cash back you earn. This makes Wealthsimple a fantastic card to use when traveling, perhaps even one of the best, as cards that have no FX fees typically only have a 1% (or 1x) earning rate.

And as a Visa card, it will also have great merchant acceptance anywhere you travel.

The Metal Card (Status Perk)

If you hold Premium or Generation status (>$100,000 in assets held with Wealthsimple), you receive a heavy metal card (similar to the American Express Platinum card). Meanwhile, core clients (those with less than $100,000 in assets) receive a plastic version of the card. This applies whether you are approved for the Wealthsimple Visa Infinite or Visa Infinite Privilege.

Of course, this is a relatively vain and intangible benefit, but I know there are those who can appreciate a good metal credit card. Furthermore, this one offered by Wealthsimple is the cheapest and the only one in Canada where the entire annual fee can be waived.

Read More: Best Metal Credit Cards in Canada

Note: If a client upgrades to Premium or Generation status after initially receiving a plastic card, they can contact Wealthsimple support to request a metal card upgrade.

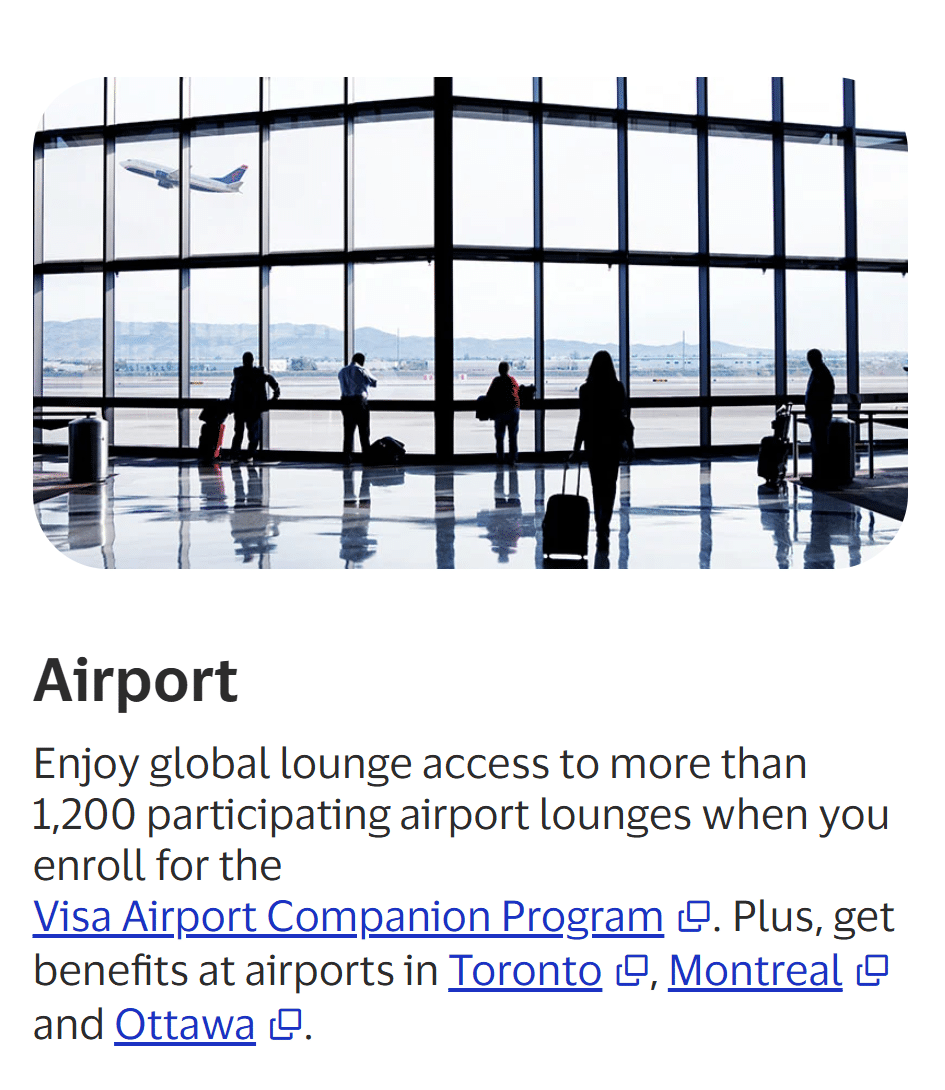

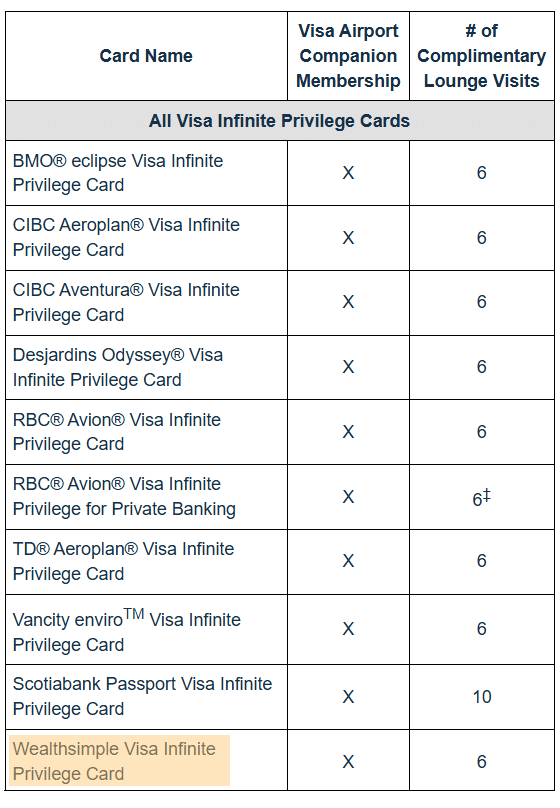

Lounge Access (Privilege Tier Only)

If you qualify for the Visa Infinite Privilege tier Wealthsimple credit card, the card comes with an airport lounge access benefit. You’ll get a Visa Airport Companion Program membership (powered by DragonPass) and six free airport lounge passes per year, allowing access to more than 1,200 lounges across the globe.

To use this benefit, you must enroll online or through the app using your card details, after which you can access participating lounges.

- Enroll: Go to the Visa Airport Companion website or download the mobile app and sign up using your Visa Infinite Privilege card to verify your eligibility.

- Access lounges: Once enrolled, show your digital membership card from the app at the lounge reception for complimentary or paid entry.

For those who are already Wealthsimple Premium or Generation clients, this is perhaps the most accessible and affordable ($0 annual fee) route to getting complimentary lounge access, as all other Visa Airport Companion eligible credit cards come with an annual fee or a temporary annual fee waiver at best.

Read More: Best Credit Cards with Airport Lounge Access

Insurance Coverage

Along with lounge access benefits, insurance coverage is another major differentiating factor between the Wealthsimple Visa Infinite and Visa Infinite Privilege. The cards both share the following insurance benefits:

- Purchase security: Protects new items you buy with your credit card against loss, theft, or damage for 90 days. You’re covered for up to $1,000 per occurrence for a total limit of $10,000 maximum per cardholder.

- Extended warranty: This warranty doubles the manufacturer’s repair period, up to an additional year.

- Mobile phone insurance: When you pay your monthly phone bill with your credit card, you’re protected against theft or damage to your mobile phone. You’re covered for up to $1,000 per claim, with a $50 deductible. You have a maximum of 2 claims per 12-month period, and you must pay your monthly phone bill with your card to qualify.

However, the Visa Infinite Privilege, as outlined in the table below, offers a stronger emergency travel medical insurance coverage, trip cancellation/interruption, and delayed and lost baggage.

| Coverage Type | Wealthsimple Visa Infinite | Wealthsimple Visa Infinite Privilege |

|---|---|---|

| Emergency Travel Medical | $1,000,000 (14 days, age <65) | $2,000,000 (14 days, age <65) |

| Trip Cancellation/Interruption | Up to $1,000 per eligible person, max $3,000 per trip | Up to $1,500 per eligible person, max $5,000 per trip |

| Delayed and Lost Baggage | Up to $1,000 | Up to $1,250 |

| Rental Car Collision/Loss Damage | No coverage | Full Coverage (up to 48 days) |

| Mobile Device | Up to $1,000 with $50 deductible | Up to $1,000 with $50 deductible |

| Purchase Security | Up to $1,000 per occurrence, max $10,000 total, 90-day coverage period | Up to $1,000 per occurrence, max $10,000 total, 90-day coverage period |

| Extended Warranty | Doubles the manufacturer’s repair period, up to an additional year. | Doubles the manufacturer’s repair period, up to an additional year. |

Most importantly, the Visa Infinite Privilege comes with rental car collision/loss damage insurance covering damage or theft of a rental car for 31 days of coverage to a maximum limit of $65,000 MSRP.

In my opinion, these insurance coverages are fairly standard, especially for the Visa Infinite tier card. But if you’re a Premium or Generation client, what you can get at the VIP tier for no out-of-pocket cost is extremely good value.

You can read more about the insurance benefits for both cards on the Wealthsimple help centre page or in the certificate of insurance.

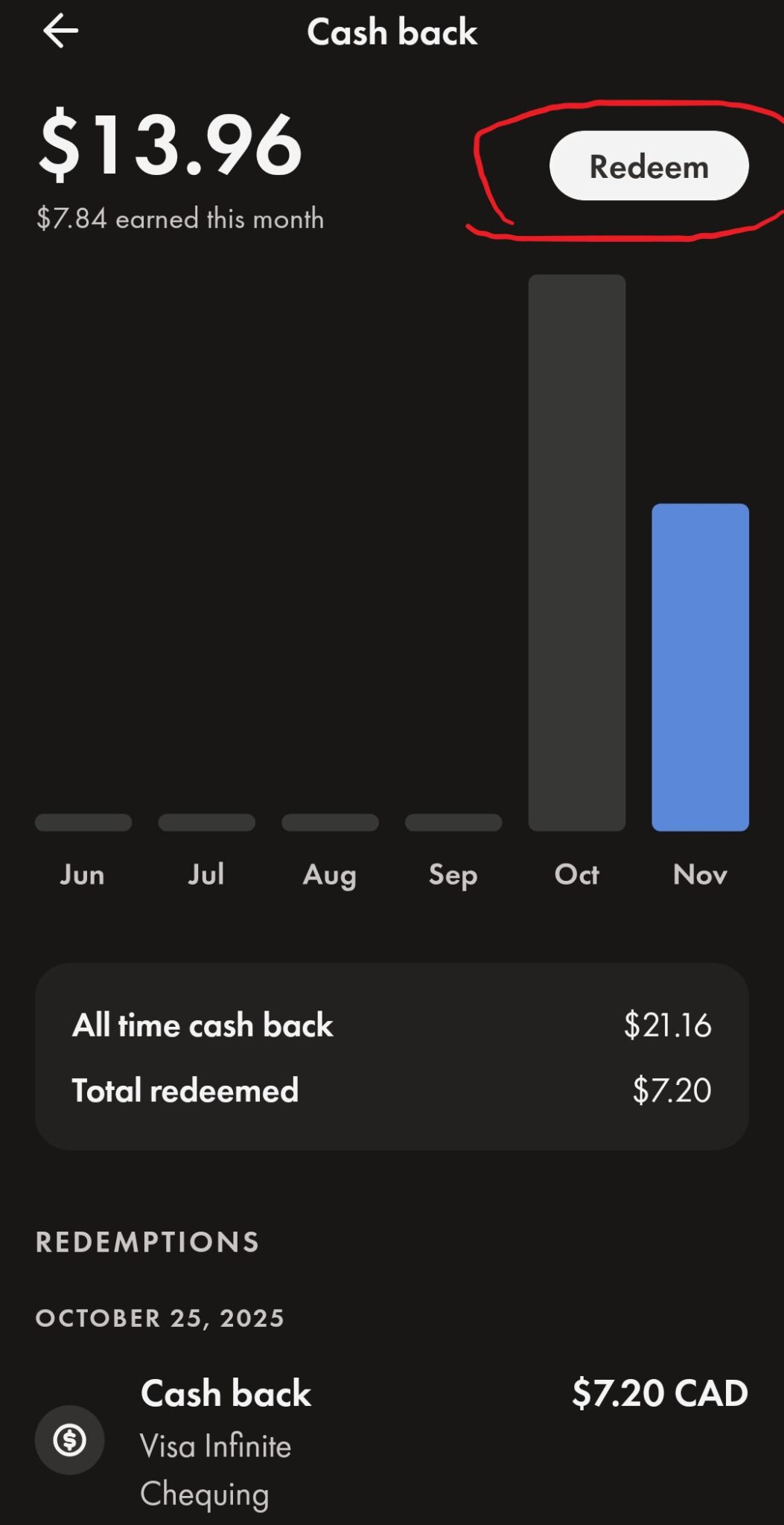

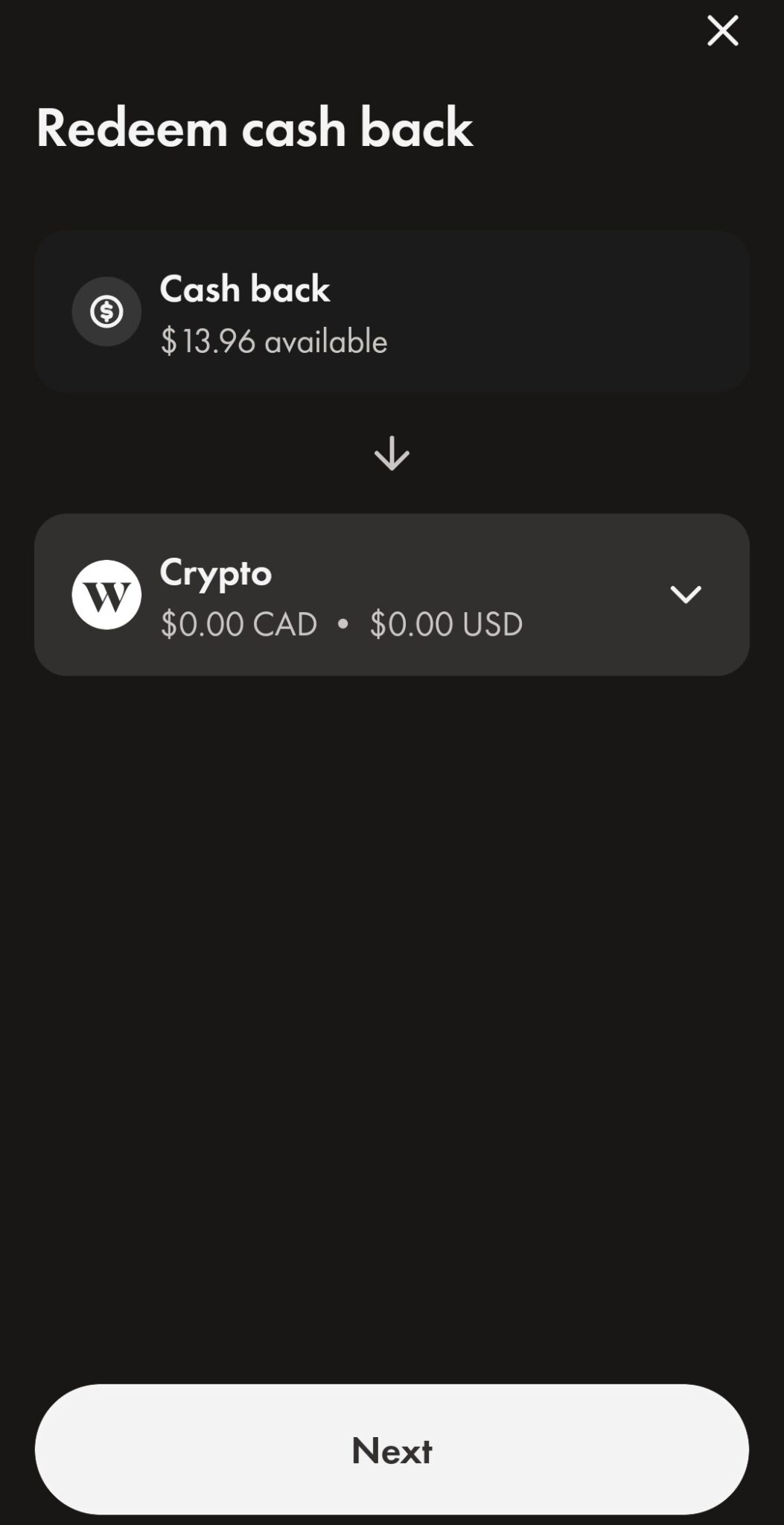

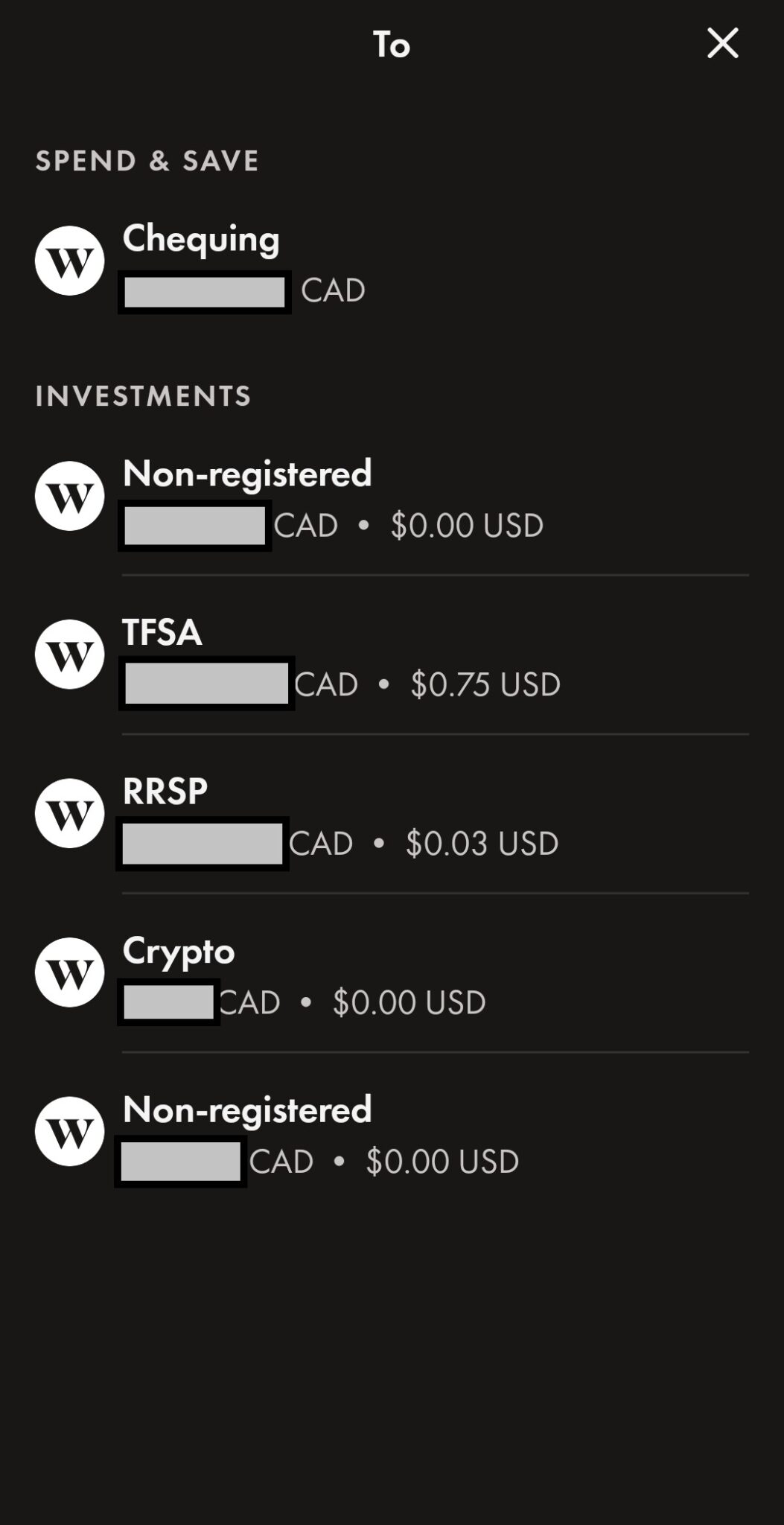

Redeeming Cash Back with the Wealthsimple Credit Card

Unlike traditional bank cards that often force you to wait for a once-a-year January statement credit, the Wealthsimple Visa Infinite offers a flexible redemption model designed to compound your earnings.

After each statement period, your earned cash back will automatically be deposited into your Wealthsimple Chequing account.

However, you can also manually initiate a redemption of your cash back on settled transactions at any time. This gives you the option to move the cash back funds into your Crypto, Stock Trading, or Managed Investing accounts, including TFSA or RRSP accounts.

Do note that cash back cannot be redeemed directly into RESP or RRIF accounts.

Comparable Credit Cards

If the Wealthsimple ecosystem isn’t for you, or if you don’t meet the asset requirements to waive the fee, here is how the card stacks up against its toughest cash back rivals.

Wealthsimple vs. Rogers Red World Elite Mastercard (The battle for flat-rate cash back)

With the Rogers Red World Elite® Mastercard, Rogers, Fido, Shaw, and Comwave postpaid consumer customers can earn 2% cash back on all eligible purchases and get a 1.5x redemption bonus on eligible Rogers, Fido, Shaw, and Comwave purchases – a 3% cash back value.

$0 cash back

$0

$0+

$0

Yes

–

The Rogers Red World Elite Mastercard is the undisputed king for anyone who subscribes to Rogers, Fido, or Shaw services. It offers 1.5% cash back on all purchases, which is boosted to an effective 3% if you use that cash back to pay your Rogers/Shaw/Fido bills.

If you are a Rogers customer, the math favors the Rogers card (3% vs 2%). However, the Rogers card charges a 2.5% foreign transaction fee, making Wealthsimple the superior choice for international travelers.

Wealthsimple vs. Scotiabank Passport Visa Infinite (The battle for No FX fees)

The Scotiabank Passport Visa Infinite+ Card is one of Canada’s best all-around travel cards, offering no foreign transaction fees and six complimentary airport lounge passes through the Visa Airport Companion Program.

Scene+ points are easy to earn on everyday spending and can be redeemed flexibly for travel, groceries, and more, making it a strong everyday carry for travellers who want simplicity and real value for $150 per year.

Earn when you apply through Frugal Flyer.

60,000 Scene+ points

$40,000

$750+

$150

No

Jul 1, 2026

Like Wealthsimple, the Scotiabank Passport Visa Infinite+ Card waives the 2.5% foreign transaction fee.

The key differentiator between the two cards is Lounge Access. The Scotiabank Passport provides 6 free lounge passes on the standard Visa Infinite tier. Wealthsimple only offers lounge passes on the “Privilege” tier, which has significantly higher income/asset requirements.

If you want airport lounge access but don’t have access to the Wealthsimple Privilege card, the Scotiabank Passport is the better buy. However, another consideration is that even though both cards have no FX fee, the Wealthsimple card will earn you a higher return on average on foreign spending, aside from grocery stores.

How to Apply for the Wealthsimple Credit Card

Applying for this card is a “mobile-first” experience. There is no desktop application; it is done entirely through the Wealthsimple mobile app.

Before you can apply for the credit card, you must open a Wealthsimple Chequing account, as this is where you will pay your Wealthsimple credit card balance from. If you don’t have one, you will be prompted to open a chequing account during the card application process.

The steps to open your new Wealthsimple credit card are as follows:

- Open the Wealthsimple mobile app and select “Open or move account” under your accounts listings

- Select “Credit card” as the account you would like to open

- Select “Apply now” to open the application

- Confirm your personal information, address, income, and other details

If you are approved, you get instant access to a Virtual Card in the app (for Apple Pay/Google Pay) while you wait for the physical metal or plastic card to arrive in the mail.

As of late 2025, the card is still in a rollout phase. You may see a “Join the waitlist” button rather than an immediate application. Wealthsimple tends to prioritize clients who already have significant assets on the platform or who have set up direct deposits of $2,000+.

A note on the Privilege card availability: While the standard Visa Infinite is becoming widely available, the Visa Infinite Privilege is currently much more exclusive. Early reports suggest that the Privilege card is rolling out slowly, primarily via invitation only to clients who already meet the “Generation” status ($500k+ assets) or “Premium” status with high income. If you don’t see the option to select the Privilege tier in the app, it is likely because your account does not yet trigger the internal eligibility algorithm.

Conclusion: Who Should Get This Card?

The Wealthsimple Visa Infinite is a “Category Killer” for one specific type of person: The Wealthsimple Investor. If you already have $100k+ on the platform, the fee waiver makes this arguably the best “catch-all” card in Canada (2% flat + No FX fee + Metal card for $0).

However, if you are not a Wealthsimple client and cannot meet the $4,000/month direct deposit requirement, the $240 annual fee makes it a lot harder to justify against the Rogers Red World Elite Mastercard (which has no annual fee at all).

If you found this review helpful, consider signing up using the link below to get started with your Wealthsimple account.

Frequently Asked Questions

Initially, no. When you join the waitlist or check your eligibility in the app, Wealthsimple performs a “Soft Check”, which does not impact your credit score. A “Hard Check” (which temporarily dips your score) is only performed if you are approved and choose to accept the card offer.

Currently, no. Wealthsimple does not support supplementary cards or joint credit card accounts. Each individual must apply for their own card based on their own income and credit profile. This is a key difference compared to major bank cards that often allow adding a spouse for a small fee.

Not directly through the Wealthsimple app. The “Bill Pay” feature in the Wealthsimple app draws funds from your Cash (chequing) account, not your credit card.

- To earn points on bills: You must pay the biller directly using your card number (e.g., Netflix, Telus, or insurance providers that accept Visa).

- For Rent/Tax: You would need to use a third-party service like Chexy or PaySimply, which charges their own processing fees, potentially negating the 2% reward value.

You must pay your bill using funds from your Wealthsimple chequing account.

- Important: You cannot currently pay the bill directly from an external bank (like TD or RBC) using the “Bill Pay” function on their site. You must first move the money into your Wealthsimple Cash account, and then pay the credit card from there.

While Wealthsimple determines your limit based on your credit profile, Visa Infinite cards typically require a minimum credit limit of $5,000. The Visa Infinite Privilege card typically starts with a minimum limit of $10,000.

The metal card is a status symbol reserved for Premium (>$100,000 assets) and Generation (>$500,000 assets) clients. If you are a standard “Core” client, you will receive a plastic card. If you later qualify for Premium status, you can request an upgrade to the metal card through support.

Reed Sutton

Latest posts by Reed Sutton (see all)

- byAir: The Ultimate Flight Tracker App? - Jun 12, 2026

- Review: TAP Air Portugal Business Class (A330-900neo) - Jun 3, 2026

- Earn Cash Back Rebates on RBC Bank Accounts - Jun 2, 2026

- BMO VIPorter World Elite: Earn 70,000 VIPorter Points & $200 FlyerFunds - May 16, 2026

- Edmonton Miles & Pints Meetup (June 2026) - May 12, 2026