In the past few years, a new credit card trend has taken the payments market by storm: prepaid credit cards. These reloadable prepaid credit cards use the payment networks of companies like Visa and Mastercard, and continue to collect fees for their issuers, but do not lend credit to customers. Instead, they’re loaded with funds directly from the cardholder.

Why would such a product exist? What are its advantages and disadvantages? And ultimately, which reloadable prepaid credit cards are the best for Canadians?

Today, let’s find out together and look at the best reloadable prepaid credit cards in Canada you might consider for a place in your wallet.

What is a Reloadable Prepaid Credit Card?

In the late 2010s, a trend made its way from across the Atlantic: the trend of prepaid credit cards. Because swipe fees are legislated to be very low in most of Europe, credit cards have never taken off there in the same way as they have in North America.

However, most societies have been getting away from physical cash and toward the ease of electronic payments. Thus, many European customers have been using debit or prepaid credit cards from fintech companies such as UK-based Revolut.

The first major reloadable prepaid credit card product to launch in Canada was the Stack Prepaid Mastercard, which offered no foreign transaction fees for cardholders. The caveat, as with all prepaid credit cards, was that funds would need to be loaded directly to the card at a merchant partner or via Interac e-transfer.

The Stack card was a hit, and buoyed by cheap credit during the COVID-19 era of quantitative easing, many fintechs in Canada and the United States proceeded to similar products at a rapid pace between 2020 and 2022.

While many of these would-be disruptors have since gone the way of the dinosaurs, many are still available to consumers, and we want to take a look at them today. The Stack card, for example, which was once on the cutting edge of no foreign transaction fees, folded back in Fall 2023.

To sum up, all prepaid cards have a few things in common. They’re supported by a smartphone app as well as a website and usually have a mobile-first approach. So you’ll need to manage your prepaid credit card from your phone primarily. Second, they all require you to load money onto the card and its backup platform. We’ll get into that more in a second.

The Value of Reloadable Prepaid Credit Cards

There are a few marked advantages to reloadable prepaid credit cards.

As we’ll see in a moment, several prepaid credit cards have features, such as no foreign transaction fees, that simply aren’t offered on many other credit card products.

There’s also the advantage that prepaid credit cards require no credit check or credit pull; they are instead open for application to all legal Canadian residents. This includes people here on temporary work or student visas, as opposed to credit cards which are often restricted to permanent residents with full-time employment.

On top of this, most prepaid cards have some sort of incentive structure (such as rewards), a feature that people without access to credit usually don’t get, and which is either unavailable or only provided at a negligible rate via debit cards.

There’s also the double-edged sword of most prepaid cards allowing you to use them like bank accounts, capable of receiving direct deposit employment income and sending Interac e-transfers at will. Most also now offer bill pay functionality.

Lastly, from a cash management perspective, the prepaid credit card acts similarly to a bank account or debit card. You can’t spend more funds than you have available, allowing for easier budgeting and restricting the ability to accrue debt.

Drawbacks of Reloadable Prepaid Credit Cards

Sometimes when I look at prepaid credit cards I wonder to myself: what unique advantage does this offer to customers other than not requiring a credit check?

The reason I wonder this is because while requiring no credit history unmistakably democratizes access to finance, there seems to be a common series of disadvantages.

First up is that because prepaid credit cards are credit cards, that utilize the Mastercard and Visa payment networks, they cannot be used at merchants that only accept debit, or for utilities and services that don’t take credit cards.

Some utilities or institutions like universities can accept bill pay, which is a service most prepaid credit cards can now provide via their app, but it doesn’t stop the prepaid credit card from being unusable at your local restaurant or barbershop that’s cash or debit only.

Secondly, there’s the entire value proposition. Most fintechs advertise prepaid credit cards as a “disruptor” to traditional finance. However, the only way to transfer money onto most prepaid credit cards is via using an old-school bank account.

How can a prepaid credit card act as a Robin Hood-like protector of the little guy against the entrenched financial system if the main mechanism to fund it is only by using traditional bank accounts? I guess you could load your employment income onto the prepaid credit card via direct deposit, but this has two risks.

The first is that if you need to do any cash transactions, it can be a major pain to get cash off a prepaid credit card. While you can still go to ATMs, many of them will charge you fees for the honor of doing so and your daily withdrawal limit is rarely enormous.

Secondly, because these products are prepaid credit cards instead of bank accounts attached to a debit card, a fraud flag could freeze your entire account. For example, if your debit card is compromised, then the physical card will be canceled, but your main chequing account will remain capable of being used.

However, if your prepaid credit card gets frozen, it is often similar to when a regular credit card is frozen. The entire account is locked out pending the removal of the fraud flag. This could prevent you from doing other basic financial transactions… which will be a serious threat if you load your employment income to your (now-frozen) prepaid credit card whence you need to pay rent.

Prepaid credit cards are also subject to all sorts of limits: load limits, cash withdrawal limits, and account limits. Say what you will about the big five banks, I can’t remember the last time they told me they wanted to put an artificial cap on the amount of my money parked in one of their accounts.

So while there are definitely advantages to reloadable prepaid credit cards based on their features, availability, and ease of use, they are not always necessarily the best solution for every consumer at all times.

Without further ado, let’s get into the four best reloadable prepaid credit cards in the Canadian market.

The Best Reloadable Prepaid Credit Cards in Canada

There are many prepaid credit cards available in Canada to choose from. However, when it comes to the best prepaid credit cards in Canada, there are five top contenders that we think are worth considering.

EQ Bank Prepaid Mastercard

The crown for the best reloadable prepaid credit card in Canada has to go to the EQ Bank Prepaid Mastercard. This is because of its ease of use and incredible features that aren’t matched in many other portions of the Canadian market. We’ve covered the various products that EQ Bank offers, but their Prepaid Mastercard is the standout amongst the crowd.

This product truly overcomes all of the hesitation I had in the previous section over potential disadvantages because it offers domestic ATM withdrawals for free, with EQ Bank remitting the ATM fees as a statement credit. Furthermore, the card offers 0.5% cashback on all transactions, both at home and abroad.

While this product does have a $10,000 deposit limit and a $500 daily cash withdrawal limit, these are still more than enough for the average Canadian.

In my opinion, the EQ Bank Prepaid Mastercard should be in the wallet of every Canadian, and especially of every newcomer or person who cannot access credit cards via traditional finance. Its features are very useful for anyone who might ever make a transaction in a foreign currency, and it just works.

You can sign up for the EQ Bank Prepaid Mastercard here.

Wise Card

The next item on our list is the Wise Card, which is a reloadable prepaid credit card using the Visa network. While this is the only Visa product that will be making an appearance, that isn’t the only way in which this card is unique.

While the Wise Card doesn’t offer anything in the way of rewards, it is quite rewarding to use because of its international flexibility.

Wise was founded primarily as a foreign currency exchange company whose goal was to get consumers a better rate on sending currency abroad. This remains their mission statement, and so getting a Wise card is a mandatory part of using Wise’s services these days.

You’ll need the Wise Card in order to transfer funds denominated in Canadian dollars from your local bank accounts and onto their platform. From there, you can then transfer this money abroad at will, such as to your US bank account.

You can also use the Wise card to store over 40 foreign currencies, making this a brilliant addition to the wallet of anyone who might travel overseas. This is of even more use if you make a lot of use of their foreign exchange service. In fact, using Wise is one of the best ways to convert CAD to USD to pay off the balance on your US credit cards.

However, if you do use the Wise card to make purchases from your Canadian dollar balance, this will only be converted at Visa’s spot rate plus a tiny fee to Wise; this is much lower than the customary 2.5% FX charged by typical credit cards.

Lastly, a nifty feature is that the Wise card can create replaceable digital cards. This is a feature common in many other jurisdictions to give users protections against potential fraud but may be the only prepaid card of its type in Canada that offers this feature.

You can sign up for a Wise account and Wise card here.

Neo Chequing Account

Next up on our list is the Neo Chequing Account. Neo, as a company, positions itself as one of the hip new cool kids, and it means that they’ve gone so far as to innovate with features new to the Canadian market.

The Neo Chequing Account offers a regular interest rate of 1.00% and unlimited transactions.

Earn when you apply through Frugal Flyer.

Savings

None

$0

The company’s main claim to fame has been in signing on a variety of vendors across the entire country as Neo partners, where people using Neo cards can expect to earn elevated rates of cashback.

As a prepaid card, the Neo Chequing Account requires no credit check and earns 1% cashback on all regular transactions plus the option to transfer to the Neo Savings Account to earn 4% interest on all balances held in that account.

The Neo Savings Account earns a minimum interest rate of 2.00% and up to 2.75% based on account balance.

Earn when you apply through Frugal Flyer.

Savings

Earn 2.25% on balances between $5,000 and $19,999, and 2.75% on balances over $20,000

$0

However, because of Neo partners, cardholders can expect to make an elevated earning rate at a variety of merchants. Be mindful, of course, of the marketing spiel: “Up to 6%” doesn’t mean that every partner pays out that much, and one of the enduring frustrations with Neo is they refuse to publicize their list of collaborators until you’ve already applied for one of their products.

Regardless of this limited transparency, this does offer one of the best earning rates available to prepaid cardholders and is a feature that only the Neo Money Account offers in addition to its regular functionalities as a prepaid card: e-transfers, bill payment, etc.

If interested, click to learn how you can get a cash back rebate on the Neo Chequing Account and earn $10 from Frugal Flyer.

Wealthsimple Cash Card

The Wealthsimple Cash Card is the option for the customer who wants the simplest, easiest-to-understand solution in a simple easy package. As usual, it’s a prepaid Mastercard.

The Wealthsimple chequing account offers unlimited free debit and Interac e-Transfer transactions with no minimum balance or monthly account fees. Account holders are entitled to unlimited free ATM transactions including third-party reimbursment. The account offers a regular interest rate of 1.25% on all deposits, with an elevated rate for premium clients and monthly direct deposits.

Chequing

Up to $

$0

Issued by the fintech Wealthsimple, which was one of the few new financial services companies to survive the pandemic intact, this card is integrated with the rest of that company’s tech platform.

When you use the Wealthsimple cash card, you earn 1% cashback on all transactions, and this is added to your Wealthsimple Cash Card balance. It can also be transferred around Wealthsimple’s app to partake of the other services they offer, such as trading using their investment accounts (both registered and non-registered).

You also don’t need to pay any foreign transaction fees, and the card charges no ATM withdrawal fees both in Canada and abroad, though you may still be subject to fees charged by the ATM operator. If you are charged a fee when using an ATM in Canada, Wealthsimple will also reimburse an unlimited number of ATM fee reimbursements (up to $5 each). Reimbursement will be made to the account linked to your Cash card within 4 business days after the ATM transaction settles

Funds sitting in your Wealthsimple Cash account also earn 3.5% interest (or 4% if you direct deposit your pay to the account), incentivizing cash to sit there, though as I said, I’d still be slightly hesitant to leave huge amounts of cash on any prepaid product.

Click to learn more about the Wealthsimple Cash account and Wealthsimple Cash Card.

KOHO Everything Mastercard

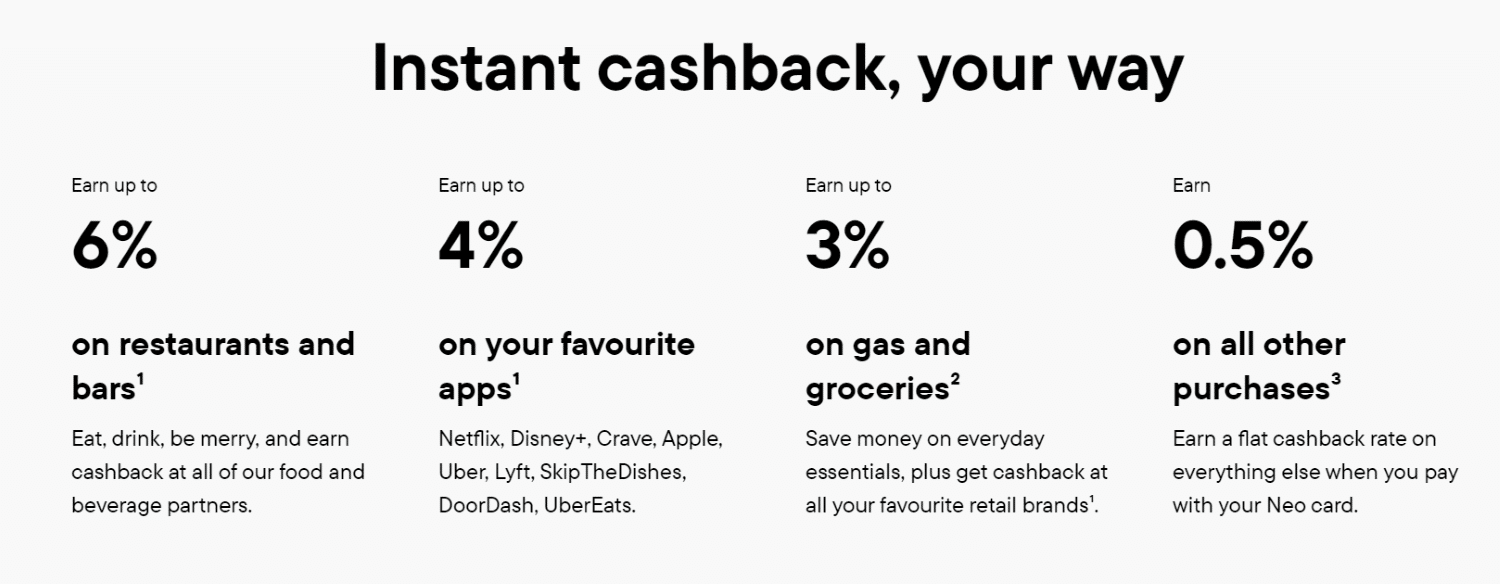

KOHO offers three prepaid Mastercards in Canada, and the KOHO Everything Mastercard is the most premium of the bunch.

The KOHO Everything Mastercard is a prepaid card that earns 2% cash back on groceries, eating & drinking, and transportation purchases, and offers a free monthly 3GB eSIM and no foreign transaction fees.

Earn when you apply through Frugal Flyer.

$20 cash back

$20

$95+

$177

No

–

There are several reasons that make the KOHO Everything Mastercard a stand-out option in the Canadian landscape. It earns cash back on all purchases, but also earns 3.5% interest on the cash balance that is held on the card.

It also offers no foreign transaction fees, which makes it an excellent card to bring and use on your travels, as you’ll save 2.5% on every transaction over a credit card that doesn’t have this benefit. Plus, cardholders will receive a free monthly 3GB eSIM that can be used in over 200 countries worldwide.

If you are interested in learning more, check out our review of the 3 KOHO Prepaid Mastercards.

Conclusion

Prepaid credit cards are now a key part of the Canadian payment landscape. While there’s been some winnowing of the field since the pandemic, with once-mighty giants such as Stack and Mogo closing shop, contenders like EQ Bank and Neo remain strong as ever.

In such a context, prepaid cards may be right for you if they offer features you need, or can help you get access to electronic payments without stringent credit requirements. Though some of the claims of the fintechs remain slightly dubious, it’s hard to dispute that some of their products offer unique and valuable opportunities to customers.

We hope that we’ve helped you choose the right prepaid today. Until next time, swipe it with ease.

Kirin Tsang

Latest posts by Kirin Tsang (see all)

- Porter Companion Pass: What You Need To Know - Jun 19, 2026

- GigSky Benefit on Visa Infinite+ Cards: What You Should Know - Jun 5, 2026

- Canadian Credit Card Tiers: What They Mean - May 29, 2026

- The Ins & Outs of Mobile Wallets - May 28, 2026

- Buying British Airways Avios: What You Need To Know - May 26, 2026

what debit card reload with credit card like buxx card in canada?

I’ve had a Neo card for a couple of years now. It started out free, but recently they started charging me $5 per month. I practically never use it, so that makes it completely not worth keeping it (which is why I’m here!).

Thanks for letting me know – $60 a year for a lacklustre prepaid credit is completely kneecapping its value proposition to the consumer.

Hello,

Just wondering can any of these prepaid cards reloadable at grocery stores (Safeway) similar to Paypower card? Also can you make bill payments with any of these cards??

Wealthsimple recently introduced to reimburse up to $5 in ATM fees for an unlimited number of transactions.