Card Summary: The Brim Financial World Elite is a new Canadian credit card ‘disruptor’. Unfortunately, their disruption is relatively non-disruptive. The card’s highlights include a competitive insurance package, no foreign exchange fees, 2% flat rate cashback on all purchases, and a newly improved and speedy customer service team. It’s lowlights are the company’s shady history and distasteful marketing of ‘$500+ first-time bonuses’ which are difficult to actually redeem for anyone living outside of Toronto.

It’s the year 2020, a pandemic is upon us, travel is on hold, people are rioting and looting in the streets, and American Express is cracking down on ‘rewards abusers’ (I personally prefer the term ‘points enthusiasts’). Now more than ever, I find the cliched phrase ‘desperate times call for desperate measures’ to be applicable. For me, these desperate measures have come in the form of … applying for the Brim World Elite Mastercard.

The Brim World Elite Mastercard is a premium credit card offering 2% back in points up to $25,000 in spend annually, 0% foreign transaction fees, and other innovative features for cardholders.

Check out our Brim Financial World Elite Mastercard review for more details.

$0 cash back

$0

$0+

$199

Yes

–

I know what you’re thinking… “what gives? Isn’t Brim Financial that company that couldn’t get their product out to applicants, then started censoring complaints on their own social media? And then when they finally got things going they raised the annual fee on their flagship World Elite card from $120 to $199?”

Yes, this is that company. But I’ve seen several data points that indicate this credit card issuer has changed for the better, at least in some aspects, since their prior mishaps. For instance, you actually do receive the card now.

On a serious level, their customer service seems to have turned a new leaf. See this Reddit user’s take on it:

“The customer service is amazing, I called this morning to ask a question about FX, and I was with an agent within 30 seconds. I have NEVER waited more than 5 minutes on hold with them. The agents are also friendly, Canadian-based, and don’t give you the run around to up-sell you, it’s straight to the point and they get everything taken care of, which I appreciate.”

But what really made me go for this card was the first year free (FYF) offer, along with the strong potential as a foreign purchasing card (no forex fee, 2% cashback), which I was in need of given the devaluation of the Rogers Red World Elite Mastercard, my previous go-to no FX card when abroad.

I’m taking the opportunity to write this post as a thorough and honest review of the Brim World Elite Mastercard credit card. I’ll comment a bit on the two lower-tiered cards, but for the most part, will keep it focused on the World Elite. Since Brim is currently (Q1 2020) offering the card with no annual fee for the first year, there is really no reason to go with the other lower-tiered cards, at least right now.

And with that, let’s dive into our Brim Mastercard review.

Features of the Brim Financial Mastercard

Brim Rewards Program

Furthermore, the Brim World Elite card awards you with ‘Brim Rewards’ points, at an earn rate of 2 points per dollar spent. Now I know what you’re thinking… “oh great, another company trying to entice me with their suspiciously printed monopoly money”. But in fact, the Brim Rewards are directly redeemable at any time for a pegged value of 1 cent per point (CPP). This means the Brim World Elite is effectively a 2% cashback credit card.

Brim has a unique digital interface where you simply swipe on the posted purchase to redeem your points. It’s very straightforward. You can also redeem the points as statement credit instead of against a specific transaction.

The Brim Mastercard differentiates Rewards points earned at this 2% cashback rate (called Base Rewards), from another type of reward called Open Rewards. We’ll discuss Open Rewards more later, but what you should know is that base rewards are capped, at a maximum of $25,000 spent per year (or $500 in cashback), while Brim Open Rewards are completely uncapped.

Of note, the other two cards, the Brim and Brim World, also earn Base Rewards but at a reduced rate of 1% and 1.5%, respectively.

A Look at the Brim Rewards Portal

Upon finally receiving my Brim World Elite card (after a long three-week wait), I was excited to take a look at the rewards portal.

Interestingly, the first thing to differentiate in the portal is two categories of offers:

- ‘inCard’ offers: Earned automatically when shopping at selected retailers with your Brim card, in-store or online, and

- ‘EShop’ offers: Credited when you click through to the retailer from the Brim portal, meaning they only apply to online purchases.

Milestone bonuses and a tiered rewards structure

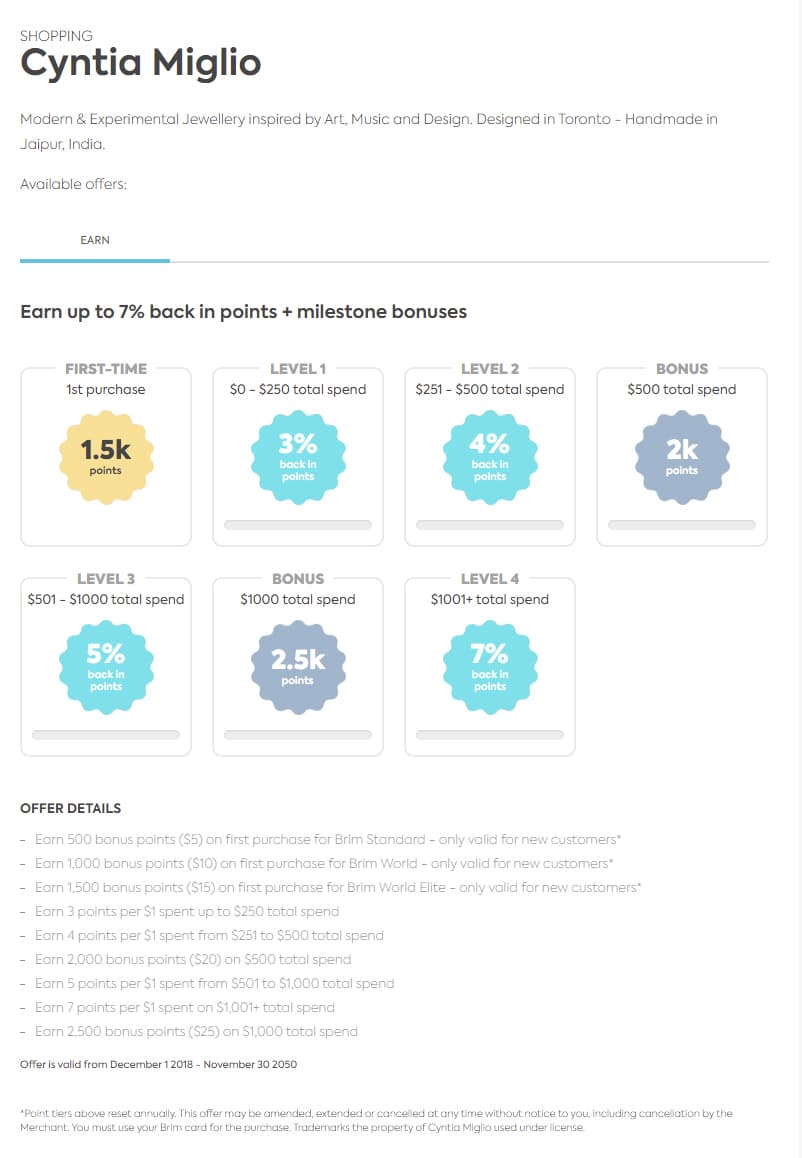

Within a particular retailer, you can see that Brim has a tiered rewards structure for many of its retailers. For example, with Cyntia Miglio, you earn only 3% back on $0-$250, but 4% on $251-$500, and even up to 7% on anything over $1,000. More importantly, there are ‘milestone bonuses’ when you spend a certain threshold, for example, 2k points ($20) for $500.

Welcome/New Client Bonus for the Brim World Elite

The welcome bonus for Brim cards is a point of confusion. Their marketing claims you can “Earn up to $500+ in first-time bonuses” (or $200/$300 for the basic and World cards). $500+ is oddly nonspecific for a welcome bonus. And what is a ‘first-time bonus’?

For Brim, a first-time bonus is a one-off bonus you can apply to a purchase from certain partner stores. For example, first purchase at Store X, get $50 worth of Brim Rewards points. These offers sometimes have conditions, and occasionally have a minimum purchase amount that must be made at the store.

Only once you have your Brim card can you view which retailers offer these bonuses. When I first logged into the Rewards portal, there were exactly 25 first-time bonus offers available to me.

Fortunately for you, I am awesome and willing to compile the entire list of the retailers offering these one-time bonuses, along with the details of the bonuses, for your viewing pleasure.

Not that the retailers and offers for Brim first-time bonuses are of course subject to change, and so may not be all exactly as listed below.

** This list is current as of June 2020.

| Retailer | First Purchase Bonus Points | Minimum Purchase | Comments |

| Indigo | 300 points ($3) | none | |

| Bloomberg | 3,000 points ($30) | Annual subscription | +20% back in points. |

| SnackConscious | 500 points ($5) | none | |

| Runner | 500 points ($5) | none | Only services Toronto |

| HelloFresh | 2,000 points ($20) | none | |

| Bag and Bougie | 2,000 points ($20) | none | +5-25% back in points |

| Province Apothecary | 500 points ($5) | none | |

| Dropbox | 2,000 points ($20) | $150 | |

| Contiki | 15k points ($150) | $800 | |

| Kobo | 1,000 points ($10) | none | |

| The Upside | 4,000 points ($40) | none | |

| Willful | 1,500 points ($15) | none | |

| Monte & coe | 2,500 points ($25) | none | +10% back in points |

| Dew Sweat House | 1,000 points ($10) | none | Toronto only |

| Life is Sweet | 500 points ($5) | none | Toronto only |

| Wild North Flowers | 600 points ($6) | none | |

| Cyntia Miglio | 1,500 points ($15) | none | |

| Graydon Skincare | 3000 points ($30) | $40 | |

| All You Are | 1,000 points ($10) | none | |

| Mary’s Brigadeiro | 3000 points ($30) | none | |

| Giftagram | 1,000 points ($10) | none | |

| HotHouse | 500 points ($5) | none | Toronto only |

| Soul Fuel | 3,000 points ($30) | none | +15% back in points |

| Poor Romeo | 500 points ($5) | none | Toronto only |

| The Wax Spot | 3,000 ($30) | none | Toronto only |

Unfortunately, you can take a glance through these offers and see that Brim has done it once again. They’ve used underhanded marketing to borderline scam their end-user. These ‘first-time’ offers are mostly measly peanuts. In addition, most of the stores are fairly niche, and several only have locations in the greater Toronto area.

It would be very difficult for the average person to extract $500 of value (as advertised by Brim) from these offers, and would likely require spending on the order of several thousand dollars.

How to Redeem Brim Rewards Points

Redeeming Brim rewards is straightforward. You simply apply your Brim points towards your statement balance, which can be done through the mobile Brim app or web portal.

See below for a demonstration of the process on the web portal.

The process is similar on the mobile app but also gives you the option to swipe right on a particular purchase to redeem Brim points against that purchase.

Other Benefits

Insurance Coverage

Brim World Elite card comes with a fairly comprehensive suite of insurance coverages, including Common Carrier Accidents, Mobile Devices, Event Ticket Protector, Extended Warranty, Purchase Protection, Emergency Medical Travel Insurance, Flight and Baggage Delay, Lost/stolen Baggage, Hotel/motel Burglary, Car Rental Collision / Loss Damage, Car Rental Accidental Death, Car Rental Personal Effects, Trip Cancellation, and Trip Interruption.

The details and amounts of coverage are contained in the table below.

| Insurance | Details | Amount |

| Common Carrier Accident | Provides coverage for accidental death or dismemberment resulting from riding as a passenger on a common carrier (land, air, or water) when the full passenger fare is charged to your card. | $150,000 per insured person up to $500,000 per accident. |

| Mobile Devices | Provides reimbursement for repair or replacement of a mobile device (smartphone or tablet), charged to your card if lost, stolen, or accidentally damaged. | Up to $1,000 for loss, theft, or damage. |

| Event Ticket Protector | Provides reimbursement for the expense of a ticket charged to your card for an event if you cannot attend for one of the covered reasons (eg. medical emergency, common carrier delay) | Up to max $1,000 |

| Extended Warranty | Automatically doubles the terms of the original manufacturer’s warranty of the covered item charged to your card, up to 1 additional year. | 2x warranty, up to one additional year and max $25,000 purchase, per cardholder |

| Purchase Protection | Protects covered items charged to your card anywhere in the world, if such item is lost, stolen, or damaged in the first 90 days from the purchase date. | 90 days $1,000 per occurrence |

| Emergency Medical Travel Insurance | Provides coverage for eligible emergency medical expenses incurred while travelling outside your Canadian province, up to a maximum of $5M per insured person, per trip. Also covers Medical Assistant services, such as finding a hospital or doctor, arranging transportation home if medically required, arranging for dependent children, etc. | 15 days if <age 65; 3 days if age 65+, coverage for $5,000,000 |

| Flight Delay | Provides coverage for reasonable living expenses such as meals, and accommodation, when your flight is delayed. Full passenger fare must be charged to your card. | $500 per day, to the max of $1,000 per occurrence for all insured. Delay must be >4h. |

| Baggage Delay Insurance | Provides coverage for the purchase of necessary clothing and toiletries when your baggage is delayed by an airline. The full passenger fare must be charged to your card. | $1,000 per insured person per occurrence, max of $2,000 for all insured. Delay must be >6 hours. |

| Lost or Stolen Baggage Insurance | Provides coverage for loss or damage to carry-on or checked baggage and personal effects while in the custody of an airline when the full passenger fare is charged to your card. | $1,000 per insured, to a total of $2,000 |

| Hotel/Motel Burglary | Provides coverage against loss or damage of personal items if a hotel/motel room is burglarized while registered as the guest of a hotel and where the room was charged to your card. | $1,000 |

| Car Rental Collision / Loss Damage | Coverage for theft, loss, or damage to rental cars up to the actual cash value of the car. Must decline the Loss Damage Waiver (LDW) or similar option offered by the car rental company and fully charge the car rental to your card. | MRSP in its model year of $65k or less, rental of 48 days or less. |

| Car Rental Accidental Death | Provides coverage for accidental death or dismemberment while riding in, driving, boarding, or disembarking from a covered rental car, provided you fully charge the car rental to your card. | Max $100,000 per insured person, up to $300,000 per accident |

| Car Rental Personal Effects | Provides coverage for burglary or damage to personal effects while such personal effects are in transit in a rental car, provided you fully charge the car rental to your card. | $1,00 per insured person, up to $2,000 per account |

| Trip Cancellation Insurance | Provides reimbursement of the non-refundable and non-transferable portion of prepaid travel arrangements charged to your card when an insured risk (such as injury, sickness, or death), occurs before you depart on your trip. | $2,000 per insured person to a max of $5,000 per trip |

| Trip Interruption Insurance | Provides reimbursement of the non-refundable and non-transferable unused portion of prepaid travel arrangements charged to your card when an insured risk (injury, sickness, or death) occurs during your trip. | $5,000 per insured person to a max of $25,000 per trip. |

How does Brim’s travel insurance stack up against other World Elite cards? Overall, it’s actually one of the most comprehensive insurance packages in Canada. Comparing individual insurances, it is on par or better than most other WE level cards.

For example, at the time of writing, the BMO World Elite card comes with a lower Emergency Medical coverage of $2M (albeit for a longer duration of 21 days), but otherwise, the trip delay, cancellation, and interruption coverages are all greater for the Brim WE. For car rental insurance, $65,000 MSRP and 48 days are also pretty standard in the industry.

The mobile device insurance (which is also included with the basic Brim card) has a depreciation clause, a deductible, plus a maximum reimbursement of $500. This does in fact cover cell phones that are partially or completely subsidized by your provider. Combined with purchase protection, it’s an attractive offer.

If you’d like to take a look more in-depth at the insurance coverage details, see this document: RSA Insurance Certificate issued to Brim Financial.

Lounge Access

The Brim World and World Elite both come with ‘Lounge Access’ through Lounge Key. Don’t get excited though because this doesn’t actually include a lounge pass, just access to be allowed to purchase a pass…. For $27 USD.

Here is the exact wording from Brim:

“What is Lounge Key? The Brim World and World Elite Cards give you LoungeKey membership and access to hundreds of exclusive airport lounges around the world, regardless of airline, frequent flyer membership, or class of ticket. Please note, it will cost you $27 USD per visit, per person. You can find more information about LoungeKey here, including the full list of accessible airport lounges around the world.”

“How do I use LoungeKey? Simply show your Brim World or World Elite card at participating airport lounges around the globe. Your card will subsequently be charged and you have access to lounges hassle-free. You can download the Mastercard Airport Experiences App to easily find participating lounges around the world.”

So it’s a bit of false marketing to call it ‘lounge access’ when it’s really just access to lounge access or ‘lounge access access’. Not a great perk, especially when a suite of other cards comes with complimentary lounge access.

Supplemental Cardholders

Cards for supplementary cardholders can be obtained for a $50 annual fee.

Eligibility

The minimum income requirement for the Brim World Elite Mastercard is the same as mandated for other World Elite tier of cards: $80,000 (personal) or $100, 000 (household).

Meanwhile, for the basic Brim card, it’s $15,000 minimum income (personal), and for the Brim World, it’s $60,000 (personal) or $100,000 (household).

Downsides to the Brim Financial World Elite Card

Brim is a new company and they are still adapting to the ecosystem. However, they do have a shady past. Perhaps the most criminal move they made was trying to conceal in the fine print the fact that they were no longer using the foreign exchange rate used by Mastercard, instead of setting their own rate.

Another small downside to the Brim World Elite is the out-of-province emergency travel medical insurance. While $5M is generous, coverage for 15 days is not a competitive duration. However, all other insurances are standard and even some such as the trip cancellation/interruption are above average for the world elite class of cards. I would still definitely read through the insurance package thoroughly if you are going to be using them (see comment above on ‘shady past’).

I would say the biggest downside to Brim is what I would now call a complete lack of a real, redeemable welcome bonus. There are numerous other World Elite offerings that can get you similar benefits, coupled with an attractive welcome bonus in cashback, points, or miles. Do not get this card if you are motivated by anything other than the insurance, no-FX, and 2% cashback.

Conclusion

The Brim credit cards are a relatively new offering in the Canadian credit card landscape. While offering first year free, their flagship World Elite offering remains a competitive no-fee foreign transaction credit card with a competitive 2% cashback on all purchases. Their insurance package is also quite competitive, and their customer service really has made a turnaround (I just requested my credit limit to be reduced via email and they responded within 2 hours with the change). This makes it an attractive card to take with you abroad.

However, outside of first-year free, you really have to weigh the value of these advantages to your personal situation. With no real welcome bonus, and cashback offerings that are easily matched by other cashback portals and mobile apps, you will be $200 out of pocket. Take a look at the other good no-FX fee card options, along with their insurance packages, and decide if the card makes sense for your situation.

Outside of first-year free, the answer for me is no.

Frequently Asked Questions

There is no real expiry, all the expiry dates are currently set to many years in the future, i.e. 2030 or 2050.

Transunion (TU) generally, but there are DPs of Equifax (EQ) hard pulls… so we’re not really sure. Mine showed up on TU.

It seems many do not receive instant approval, instead receiving an ‘application in process’ message and follow-up email. You should receive an email asking for a utility bill or proof of address/ID and then final approval about a week later.

Through the mobile app or website, as a statement credit.

100 points, or $1.00.

Yes, you can.

No, according to the Brim team, “to be eligible for Brim Rewards, you must pay directly with your card at that merchant, not through Paypal.”

In theory, if you use your card with an eligible inCard retailer that is also on a cashback site, you could double-dip. However, I’ve observed that most of the inCard retailers are not available on cashback portals.

Reed Sutton

Latest posts by Reed Sutton (see all)

- byAir: The Ultimate Flight Tracker App? - Jun 12, 2026

- Review: TAP Air Portugal Business Class (A330-900neo) - Jun 3, 2026

- Earn Cash Back Rebates on RBC Bank Accounts - Jun 2, 2026

- BMO VIPorter World Elite: Earn 70,000 VIPorter Points & $200 FlyerFunds - May 16, 2026

- Edmonton Miles & Pints Meetup (June 2026) - May 12, 2026

Stay away from this card if you’re a low-risk big spender: when we found out that MBNA was removing its 2% cash back to go to “categories” on August 31st 2021 (where Costco is in the “other” category at 1%), we knew that it was time to move on to another card as we are big credit card spenders (>$5000/month) that always pay on time on the last day of the month (hence, the kind of clients that would keep Brim’s cash flow going with MasterCard but that would not make them much money in interest as we always pay on time).

The application process was OK (after a few bugs that got cleared once the history on my browser was cleared) and we were quickly approved for… $5000 per month!

After laughing for a while, we sent in proof that our credit limits on our other cards are all at least 5 times this amount and that $5000 was insufficient for my upcoming trip to Europe as I travel a lot for business. (remember that the $5000 limit still remains until you pay at the end of the NEXT billing cycle so for someone like us that only pay at the end of the month, that $5000 limit is pretty much half… and there is no way that I’m going to pay ahead of time as BRIM is the service, not the other way around so it is up to THEM to cater to MY needs… not to me to cater to their needs – it kind of reminds me of a certain Capital One credit card from that large warehouse store that represents more than 50% of our purchases…)

The result?

They refused to increase our limit. As a result, we have been receiving “credit card declined” messages for the last 2 weeks. It’s not a problem as we still have other credit cards but in the end, it made us realize that it made no sense to pay $250 per year for a credit card with a $5000 limit per month, especially when we found out that the only “perk” that could have given it some residual value would have been worldwide access to lounges when we travel via another airline… which we found out that we have to pay for! (Which regular world traveler does not already have access to world lounges via their miles already? This is thus just a fake marketing plot to highlight a benefit that isn’t really one.)

Now, I could go on as to what is wrong with this card but I will reserve judgement because this year’s fees for the primary credit card were free (but not the secondary card at $50). So far, this card has proven not to be useful to us and I have a series of emails that clearly shows that they have no interest in fixing our limit for the type of customer that I am (i.e. big spender that always pays on time). Hopefully they will adjust within the coming months because it’s clear to me that they have misunderstood something in their target clients: only someone that does not know how to manager money will pay $250 for a $5000 credit limit and people with money don’t want to have to “manage” the cash back on their credit cards. We just want a credit card that works everywhere. Not catering to those clients will mean they’ll end up with people that don’t know how to manage their credit cards…. (i.e. bad debts, of course… so expect that after a few years, Brim will probably suffer the same fate as Capital One… that last company that gave us an $8000 credit limit until Costco intervened and they fixed it upwards…)

So, do I need to tell you whether I’ll be using their card when we reach their $25,000 yearly threshold where the cash back reverts from 2% down to 1%?

Hummm, the answer for me at this stage is that I am not sure yet which credit card I’ll be using as I will go with whatever Costco decides but, unless they fix my situation, I already know that my answer will be “NOT Brim”.