The opinions expressed in this article are solely those of the author, and do not constitute investment advice, legal advice, or tax advice. As always, do your own research and invest at your own risk.

Introduction: Good Debt vs. Bad Debt

On the topic of personal finance, It has been said that there is ‘good debt’ and ‘bad debt’. Bad debt is what we typically think of with debt – overdue credit card payment, payday loans, high-interest rates. Good debt on the other hand is debt that is typically low interest, and that we expect to use to somehow accrue value or make a net positive return.

A mortgage (particularly a cash-flow positive rental property), is a great example of using leverage to earn income or increase your net worth through capital appreciation. But one less discussed debt which I would argue is good when used properly, comes from credit card balance transfers. As we’ll discuss, these can essentially act as a very low-interest loan, on the order of 1-3%.

Alternatively, unsecured lines of credit (uLoC), home-equity lines of credit (HELOC, see the Smith Maneuver), or even investment-secured lines of credit can provide relatively low-interest rates.

For the purposes of this article, however, we will mostly focus on balance transfers. I personally feel that any loan with interest above 4-5% may not be worth the downside risk. This can be debated depending on one’s income and tax situation (investment loan interest is a tax write-off for example), but such discussion is outside the scope of this article.

Balance Transfer Basics

A balance transfer is a special promotion interest rate offered on a credit card to entice you to transfer your balance from another bank/product. With a balance transfer, your annual interest rate (APR) will be much lower than the average market rate, with rates as low as 2%, 1.9%, or even 0% APR for a set duration of time, usually anywhere between six and 12 months.

Some banks only allow you to use your new promotional card to pay off another high-interest credit card you were carrying a balance on, however most in Canada operate similar to a line of credit, even allowing you to transfer the totality of your approved credit limit as cash to your bank account.

So, what’s the downside to balance transfer? An interest-free loan sounds too good to be true, doesn’t it?

Well, yes to some extent. There are some stringent conditions and rules that you need to follow. We’ll cover some of them generally here, but I would always recommend reading the T&Cs of the balance transfer offer before accepting it.

Transfer Fee

Most promotional offers will have a balance transfer fee that you must pay at the same time you make the transfer. This is typically 1-3% of the total amount you borrow.

There’s no way to get around these fees, but 1% of the principal for a 10- or 12-month balance transfer is lower than inflation and certainly lower than any bank’s competitive lending rates.

Also, because this fee will be charged at the same time as the initial transfer, make sure you don’t try to transfer your entire credit limit. Otherwise, you will end up going over and being charged fees for the overage. A good rule of thumb is to borrow 5-10% under your credit limit for a balance transfer. So if your credit limit is $10,000, borrow $9,000-$9,500.

Proportionate Allocation

Proportionate allocation is a dirty tactic that can be used by banks to turn balance transfers against you. When you make a credit card payment, your credit card issuer has a choice of how it can allocate your payment among the various balances on your card.

For example, on one card you may have a balance of 0% from a balance transfer, 19.9% from a purchase and 24% from a cash advance. Of course, you would like the highest APR to be paid first, but banks often choose to pay off each proportionate to each rate’s balance: proportionate allocation.

In effect, if your card uses proportionate allocation methodology, you will be charged high APY interest on any purchases made outside the balance transfer’s principal unless you pay off the entire balance of the card including the balance transfer amount.

You can read the fine print to determine how your bank handles this if you want. Some balance transfer offers also offer the same rate on purchases. But my approach and the approach I recommend to anyone using balance transfers: do not ever under any circumstances make any purchases on your card.

After your balance transfer funds are transferred, don’t touch the card except to make your monthly principal payments if applicable (more on these later).

Principal Payments

As with credit card purchases, balance transfers still have a minimum payment towards the principle amount each month. Typically this is a minimum of $10 or a percentage of the balance (1-3%). You will see this on your first statement (which will also include the initialization fee).

Always pay off these little monthly balances on time. Failure to pay on time will probably lead to late fees and your promotional rate may even get pulled.

Finally: remember that there is often no grace period on balance transfer offers.

While some companies will offer you 21 days interest-free after your last statement with the promotional interest rate cuts, it’s best to pay off your balance transfer before the final statement. Some companies will charge you the traditional 22.99% APR cash advance rate the moment that the last statement is printed.

Whether to pay the minimum or more than the minimum, is a personal decision for you to make. I pay the minimum so as to maximize my return on capital, but I always have a plan for how I will pay the full lump sum at the end of the promotional period. We’ll discuss some advanced strategies such as using a line of credit to bridge successive balance transfer offers a little later.

So to summarize: follow these simple rules for balance transfer success:

- Borrow a maximum of 90-95% of your total available credit limit

- Never make any purchases on your balance transfer credit card

- Be wary of monthly principal payments and pay them on time

- Have a plan for paying off the card at the end of the promotional period

Best Balance Transfer Offers

Canadian Credit Cards

For a complete up-to-date list of the best balance transfer credit card offers available in Canada, please see our latest article: Best Balance Transfer Credit Card Offers in Canada. A few of these offers are also highlighted below.

CIBC Select Visa

The CIBC Select Visa card is a low annual fee credit card with low purchase and cash interest rates, and a promotional balance transfer rate of 0% for 10 months (1% transfer fee).

0 None

$0

$0+

$29 (FYF)

Yes

–

Another formidable balance transfer opportunity is the CIBC Select Visa Card, which offers 0% interest for 10 months with a 1% transfer fee. Unfortunately, this offer is only available at the time of applying and imposes a limit of 50% of your approved credit limit. Therefore it may or may not be worth it for you to apply unless you have a strong suspicion you will be approved for a large credit limit.

If you already have a few credit cards with CIBC, you may be better off waiting or inquiring about a targeted/rotating balance transfer offer on one of your existing cards. See below.

CIBC Targeted Offers

CIBC offers competitive but non-public balance transfer promotions. Usually, these are targeted (you should receive the offer in your online portal or while on the phone with customer service, perhaps while doing a product change. The rates can vary but are commonly 0% APR for 10 months with a 1-2% transfer fee.

CIBC’s policy is typically to only offer 50% of the credit limit as a transfer (the so-called ‘cash limit’), however, there are data points of people asking and being allowed to do the full limit. Recently I was offered a BT where my cash limit was the entire balance.

Furthermore, even if you haven’t been targeted, you may try to call in and talk to the supervisor to get a balance transfer promo applied to your account manually.

RBC Cash Back Mastercard

The RBC Cash Back Mastercard earns up to 2% cash back on grocery purchases and 1% cash back on all other purchases.

$70 cash back

$1,000

$70+

$0

Yes

Sep 9, 2026

This offer, only available through a special top-secret link, provides 1.9% APR for 10 months, but with no transfer fee, which is definitely a decent offer to consider.

RBC offers this rate on both balance transfers and cash advances. So you can use this card effectively as a line of credit for 10 months.

Other Options: BMO, RBC, PCF

There are lots of other balance transfer options available, from the likes of BMO, RBC, PC Financial, and others. These are usually in the range of 2-3% APR or transfer fees. I would exhaust your options with MBNA and then CIBC before going for any of these, personally.

US Credit Cards

The Holy Grail of Balance Transfers: 0% APR, 0% Transfer Fee

As with credit cards and many other financial products, the USA tends to have a greater and more competitive selection of balance transfer offers than Canada. In fact, offers of 0% APR and 0% transfer fees are not unheard of.

Federal Credit Unions

Aside from American Express, the only other 0% APR / 0% transfer fee offers I’ve come across are from Federal Credit Unions. Disclaimer: I have no personal experience with these credit unions. However, as far as I can tell they are publicly available offers with relatively flexible eligibility criteria.

La Capitol FCU

0% APR for 12 months, with 0% transfer fee. Additionally, this card even has no over-the-limit fee and 0% APR on purchases for 12 months. They appear to accept applications from ITIN holders and non-residents but this is not confirmed.

Wings Financial Visa Platinum

0% APR for 12 months, with 0% transfer fee. You will need to provide SSN or Green Card along with proof of US address (utility bill).

First Technology FCU Choice Rewards Mastercard

0% APR for 12 months, with 0% transfer fee.

There are also rotating 2.99% BT promotions available for existing cardholders.

Other Options: Citi, Bank of America

Aside from Amex and FCU, most major banks offer a standard 0% BT card with a 3% transfer fee. This can still be worth considering, especially if you already have a good relationship with the bank and high available credit limit on pre-existing tradelines. See the below table for some of the available options and balance transfer rules of different banks.

You will note that in this table I highlight the ability to consolidate credit lines (also known as reallocation). We’ll get into this later on when we discuss ‘churning balance transfers’, however, the idea is that you establish a credit line at an institution that you can later use to supplement future repeat/additional balance transfers to increase your total available credit line each year.

| Institution / Credit Card | Interest Rate | Transfer Fee | ID Requirements | Funds Transfer Method | Able to consolidate credit lines? | Maximum Transfer Amount |

|---|---|---|---|---|---|---|

| La Capitol FCU Rewards Visa Card | 0% for 12 months | 0% | SSN or ITIN | EFT or check | 100% of credit limit | |

| Wings Financial Visa Platinum | 0% for 12 months | 0% | SSN or Green Card | |||

| First Tech FCU ChoiceRewardsWorldMastercard | 0% for 12 months | 0% | SSN only | EFT or credit card | 100% of credit limit | |

| Citi Diamond Preferred Card | 0% for 18 months | 3% | SSN or ITIN | Credit card or check | Yes | 100% of credit limit |

| Citi Simplicity Card | 0% for 21 months | 3% | SSN or ITIN | Credit card or check only | Yes | 100% of credit limit |

| BankAmericard Credit Card | 0% for 18 months | 3% | SSN or ITIN | Yes | 100% of credit limit | |

| Wells Fargo Platinum card | 0% for 18 months | 3% | SSN only | Yes | ||

| U.S. Bank Visa Platinum Card | 0% for 20 months | 3% | SSN only | No | ||

| Discover it Balance Transfer | 0% for 18 months | 3% | SSN only | Yes, subject to hard inquiry and CL increase | ||

| TD Cash Credit Card | 0% for 15 months | 3% | SSN only | Check to institution | 100% of credit limit |

How to Generate Alpha (Returns)

So you’ve been approved for your shiny new balance transfer offer, line-of-credit, or other smart debt vehicles. What now?

The traditional use of a balance transfer is to reduce high APR interest payments from another credit card or loan – debt consolidation. But that’s not what we do here, because we’re frugal and we don’t have that kind of debt to begin with.

Ultimately the best way to generate a return from balance transfers will depend on your own personal situation, risk tolerance, and time horizon. I am by no means a financial advisor or expert. However, I can provide you with some ideas that I considered when I recently started utilizing balance transfers and LOCs.

Intuitively you should have a lower risk tolerance when you’re using money that is not your own. This is why I’d recommend low risk avenues like high interest savings accounts, market index investments, and if you’re inclined, stablecoin or crypto staking (higher risk).

High Interest Savings Accounts

In a high interest rate environment, like we have had post COVID-19, you can secure a solid return just by depositing your money into a high interest savings account.

For example, with the Wealthsimple Cash account, you can earn 4-5% interest just by holding cash in the account, and its completely liquid free to withdraw at any time.

There are a handful of other Savings Accounts in Canada which offer promotional savings rates of 5% or even 6% on deposits for a limited period of time.

You can combine these type of accounts with bank account sign-up bonuses, usually offered on checking accounts, which give you $300, $400, or even $500 cash one time for opening a new account.

These types of accounts can be a fantastic, risk-free way to earn a return on your free cash or cash you’ve acquired through a balance transfer, for example.

Stock Market Investing

A more traditional method to generate alpha is of course investing in equities/stocks through your brokerage of choice. If you don’t already have one, I recommend Wealthsimple Trade or Questrade, which offer either free commissions on trades or free commissions on ETF buys, respectively. This makes it easy to rebalance your portfolio whenever new money flows in, no matter the denomination.

I am by no means an expert investor, so take everything that follows with a grain of salt. When it comes to investing my own money, I tend to select riskier investments as I have a long time horizon, desire more aggressive growth and can handle larger drawdowns in the short term.

However, when I began investing using borrowed money from loans/balance transfers, I felt the need to research lower risk (lower beta) portfolios that still produce modest returns. I wanted investments with a lower downside in the worst-case scenario that I needed to sell the investments to cover the loan.

Thus far, I have found three investment vehicles that better suit my risk tolerance for borrowed money: model portfolios, low-volatility ETFs, and covered call ETFs.

Model Portfolios

‘Model Portfolios’ are one-and-done style ETF investments that provide a balanced index portfolio in a single ETF. You choose a risk profile or equities-to-bonds ratio of 20%, 40%, 60%, or 80%, and the ETF holds the corresponding amount of equities and bond ETFs, balanced across Canada, USA, ex-North America and emerging markets.

Two of the most prominent sets of model portfolios are offered by Vanguard and iShares, discussed in-depth on Canadian Couch Potato. The TD e-Series funds mentioned on Canadian Couch Potato may also be worth considering if you plan to open an investment-secured line-of-credit (iLoC) with TD. This is because TD requires you to secure the loan with their own investment products…

There are also some good ETF Model Portfolio suggestions created by Dale Roberts of CutTheCrapInvesting.com, for those interested.

Low-volatility ETFs

Low-volatility ETFs on paper, seem too good to be true. You can own a diversified bag of equities with an ETF like ACWV/XMY or SPLV, which carefully choose from a broad universe of high quality stocks, those that have lowest volatility.

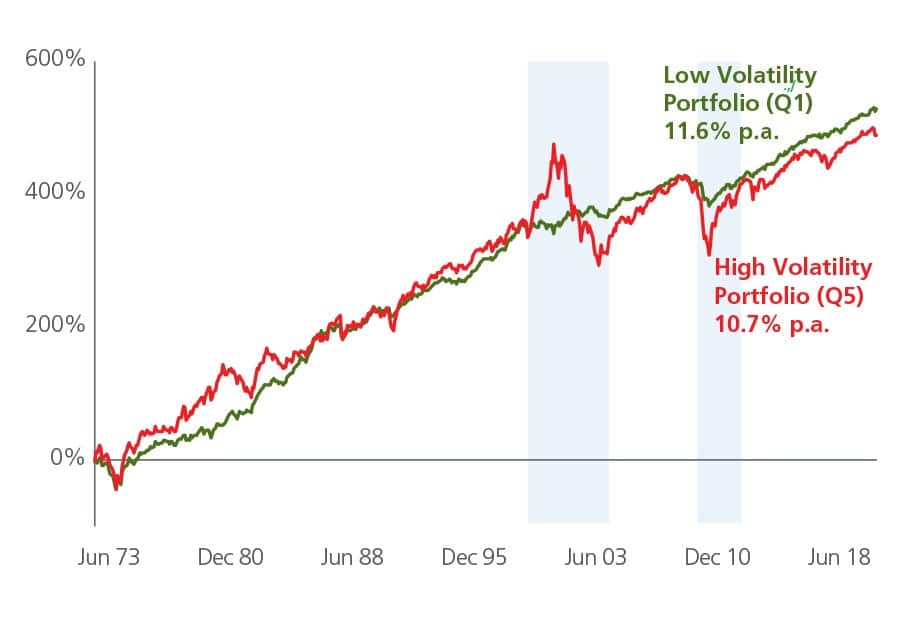

Yet in looking at historical performance, the returns don’t seem to subpar to the benchmark index. There is some theory behind this: the low-volatility anomaly is an observation that “low-volatility stocks have higher returns than high-volatility stocks in most markets studied”.

Of course, even if the ETF produces the same or very similar level of performance to the overall market while having lower relative volatility, it has done its job successfully.

Low-volatility ETFs generally use one of three methodologies to select holdings from a broad universe of stocks:

- Classify eligible securities by their beta index, which measures their sensitivity to general market fluctuations. Those with the lowest beta are selected and also weighted proportionally to their betas. See BMO Global Asset Management ETFs.

- Measures the risk of eligible securities based on standard deviation of returns over a period of up to three years. Weighting is also inversely proportional to standard deviation. See Invesco and CI First Asset ETFs.

- More complex strategy that uses an optimization algorithm to select and assign a weight to shares from the universe of eligible securities while also factoring in their correlations. In accordance with a number of diversification constraints, the algorithm proposes securities and weights that collectively produce the lowest volatility. See iShares ETFs.

Of course low-volatility ETFs do come with downsides. For one, they are costlier than basic ETFs. They can also be biased towards particular sectors. For example, ACWV/XMW has a bias towards consumer staples and healthcare, while SPLV/ULV is comprised of more than 30% utilities.

Some prominent low-volatility ETFs are included in the chart below, for informational purposes.

| MARKET | MCAP | AVG VOL | DIV (%) | RETURN (%) | 5R BETA | MER (%) | |

| VVO – Vanguard Global Minimum Volatility ETF | Global | 47M | 1K | 2.13 | 5.30 (3 yr) | 0.91 | 0.40 |

| ACWV – iShares Edge MSCI Min Vol Global ETF (See also: XMW) | Global | 5.3B | 329K | 1.66 | 9.07 (10 yr) | 0.63 | 0.20 |

| PLV – Invesco Low Volatility Portfolio ETF | Global | 34.12M | 2.14K | 2.12 | 4.69 (5 yr) | 0.66 | 0.39 |

| ZLB – BMO Low Volatility Canadian Equity ETF | Canada | 2.7B | 56K | 2.51 | 9.74 (10 yr) | 0.74 | 0.39 |

| FCCL – Fidelity Canadian Low Volatility Index ETF | Canada | 14.6M | 410 | 3.09 | – | – | 0.40 |

| TLV – Invesco S&P Composite Low Volatility Index ETF | Canada | 315.98M | 6.8K | 1.93 | 6.99 (5 yr) | 0.67 | 0.34 |

| ZLU – BMO Low Volatility US Equity ETF | USA | 1.6B | 8.6K | 1.83 | 10.00 (10 yr) | 0.60 | 0.33 |

| ULV.F – Invesco S&P 500 Low Volatility Index ETF | USA | 212M | 1.8K | 1.55 | 9.45 (10 yr) | 0.89 | 0.31 |

| ZLI – BMO Low Volatility International Equity ETF | ex-NA | 390.57M | 4K | 2.62 | 5.87 (5 yr) | 0.72 | 0.45 |

| IDLV – Invesco S&P International Developed Low Volatility ETF | ex-NA | 759M | 168K | 2.20 | 4.04 (5 yr) | 0.70 | 0.25 |

| ZLE – BMO Low Volatility Emerging Markets Equity ETF | Emerging | 111.15M | 600 | 2.17 | 0.36 (3 yr) | 0.80 | 0.45 |

| EEMV – BTC iShares Edge MSCI Min Vol Emerging Markets ETF | Emerging | 3.88B | 255K | 3.42 | 6.98 (5 yr) | 0.74 | 0.25 |

| EELV – Invesco S&P Emerging Markets Low Volatility ETF | Emerging | 322M | 137K | 2.42 | 5.48 (5 yr) | 0.85 | 0.30 |

Covered Call ETFs

Covered call ETFs are a broad class of ETFs that employ a strategy that uses covered calls. A covered call is a type of stock option, where you hold a stock, but sell the right to someone else to purchase it from you at a specified price within a certain time frame.

Covered call ETFs seek to generate income on a basket of equities while providing some downside protection. They have higher dividend payouts from the premiums they make through selling calls. However, this strategy means that covered call ETFs may underperform the underlying equities in an upward moving market.

| Pros of covered call ETFs | Cons of covered call ETFs |

| According to a study commissioned by the CBOE, a strategy of buying the S&P 500 and selling at-the-money covered calls slightly outperformed the S&P 500. | In a rising market, and especially a rapidly rising market, your returns will be hampered by the ETFs obligation to sell some shares potentially below market value to fulfill their options obligations. |

| Partly due to the increase in returns when market volatility is high, a covered call approach is usually less volatile than the market itself. | In the long term, covered call ETFs tend to underperform their non-covered counterparts, and take longer to recover after a crash. |

| Covered call ETFs make a relatively complicated and fairly profitable options market strategy easily accessible to average investors. | Covered call ETFs have higher management fees than basic ETFs, because they have to manage their options positions in addition to the equity holdings. |

I’ve included a table of some covered call ETFs that have caught my eye. Again, this is purely for informational purposes. These are examples, not endorsements.

| ETF | MARKET | MCAP | AVG VOL | DIV (%) | RETURN (%) | 5R BETA | MER (%) |

| ZWC – BMO Canadian High Dividend Covered Call ETF | CAD | 1.08B | 225K | 7.15 | 5.71 (3 yr) | 0.89 | 0.72 |

| ZWB – BMO Covered Call Canadian Banks ETF | CAD | 2.19B | 122K | 5.21 | 8.93 (10 yr) | 0.94 | 0.72 |

| CIC – CI Canadian Banks Income Class ETF | CAD | 194.04M | 25K | 7.96 | 9.55 (10 yr) | 0.96 | 0.80 |

| FHI – CI First Asset Health Care Giants Covered Call ETF | USA | 127.75M | 3.81K | 9.81 | -* | -* | 0.72 |

| NUSI – Nationwide Risk-Managed Income ETF | USA | 292.89M | 148K | 7.70 | -* | -* | 0.68 |

| JEPI – JPMorgan Equity Premium Income ETF | USA | 1.08B | 420K | 8.07 | -* | -* | 0.35 |

| QYLD – Global X NASDAQ 100 Covered Call ETF | USA | 2.92B | 1.8M | 11.99 | 11.19 (5 yr) | 0.72 | 0.60 |

| RYLD – Global X Russell 2000 Covered Call ETF | USA | 174.33M | 152K | 10.58 | -* | -* | 0.60 |

| XYLD – Global X S&P 500 Covered Call ETF | USA | 295.19M | 102K | 8.46 | 8.74 (5 yr) | 0.80 | 0.60 |

-* not enough data.

Crypto Stablecoins or Crypto Staking

Stablecoins are the answer to the frequent criticism of cryptocurrency volatility. There are a variety of approaches to stablecoins, but the simplest approach is 1:1 backing with fiat currencies. Eg. a company mints an ERC-20 token for each USD sent, and so holds 1 USD for each digital USD token created. This is the approach used by Tether USD (USDT), True USD (TUSD), and most cryptocurrency exchanges that have their own stablecoins (Gemini’s GUSD, Coinbase’s USDC, Binance’s BUSD).

Once you hold one of these stablecoins, you are a participant in the cryptocurrency ecosystem. Different institutions and protocols will allow you to hold your stablecoins with them and provide you with an APY interest rate (paid out daily, weekly, or monthly) in return.

The business models are various but mostly revolve around the fact that institutions and individuals entrenched in crypto often need fiat-like currency/cash but want to maintain their cryptocurrency positions, and so take loans in stablecoin using their cryptocurrency as collateral. This is why interest rates on stablecoins are higher during bull markets, where selling pressure on cryptocurrency is much lower. Exchanges themselves also need to be able to provide liquidity on their stablecoin trading pairs.

We won’t dive too deep into crypto-economics in this post, but the bottom line is you can hold a USD-pegged digital currency and make ~5% return on your investment with relatively low risk. You can choose to hold stablecoins on various exchanges, or on independent platforms.

Churning (Bridging) Multiple Balance Transfers

At the end of the balance transfer period, you will be responsible for paying off the remaining balance in full. As I mentioned earlier, before you even accept a balance transfer, you should have a plan for how you will pay it off.

If you’ve invested in something where the principal is guaranteed and liquid (eg. stablecoin yields), then you have the option to pay off the balance with the original funds. But for most investment types, even equities which are only semi-liquid, you should have a backup plan.

One strategy I employ is to have a line of credit available. This can be a HELOC, an unsecured LOC, or the like. At the end of the balance transfer period, use the line of credit to pay off the balance. You can then float the low (and tax-deductible) interest payments until you can secure another balance transfer.

Let this be known as “balance transfer churning”!

I find it is especially effective when you’re investing in equities. Statistically, the longer time you remain in the market, the greater likelihood your investments will be profitable. Balance transfer churning allows you to remain invested for longer (maybe indefinitely).

A Few Words of Caution

For people who understand and manage credit responsibly, balance transfers can be a useful tool for wealth accumulation. That being said, borrowing always comes with some inherent risk.

As mentioned, liquidity risk is one thing to be aware of and plan for. Know your time horizon for the loan.

Furthermore, be aware that this will likely impact your credit score, and will increase your debt service ratios. For this reason, I would hesitate to take out a large balance transfer right before applying for a mortgage to purchase a home for example.

If you are unsure whether it’s right for you, it’s best to discuss further with a qualified financial advisor, accountant, or another knowledgeable party before proceeding.

Frequently Asked Questions

This is definitely something to think about first and will depend on your personal financial circumstances.

Generally, a line of credit will be higher interest than a balance transfer. However, interest rates for HELOCs can be very close, and depending on the value of your home, HELOCs also provide you with more available credit. Lines of credit don’t have a short time frame to pay down like with balance transfers either.

Additionally, because a LOC used for investing is tax-deductible, those making high income could actually have a lower effective interest rate on a HELOC than on a balance transfer. But for most mid-to-low income earners, a balance transfer will still likely work out cheaper.

Smith Maneuver is an advanced tax strategy to convert interest paid on a personal residence, which is not tax-deductible, into tax-deductible investment loan interest. This method requires a readvanceable mortgage (mortgage bundled with a LOC that grows with each mortgage payment).

For each mortgage payment the same amount is borrowed under the LOC and invested, resulting in 1) a hopefully higher rate of return than the interest, and 2) a tax refund at the end of the year that can be repaid to the mortgage. Read more about the Smith Maneuver here.

A balance transfer will potentially negatively affect your credit score, but it depends. A balance transfer appears similar to a maxed-out credit card. Credit utilization is a large component of your credit score. If you have $50,000 total available credit and a balance transfer of $30,000 (60% utilization), it is going to hurt your score, no question. However, if you have $100,000 available credit and a balance transfer of $10,000 (10% utilization), the effect should be rather minimal.

Generally, you should still be able to apply for new credit cards just fine. But do keep this in mind if you’re applying for a mortgage, vehicle financing, or an unsecured line of credit. It may raise eyebrows and be something you need to explain to the lender.

A line of credit will appear on your credit reports as a new account. If you never use your available credit or only use a small percentage of the total amount available, it may lower your credit utilization rate and actually improve your credit score. On the other hand, if you borrow a high percentage of the line, that could increase your utilization rate, which may hurt your credit score.

Generally no you cannot transfer a balance from a card at one institution to a card at the same institution. Balance transfers are intended to entice new customers with low interest rates, not reward existing customers who have debts.

The best balance transfer credit cards in Canada are subject to change, but currently a close tie between the CIBC Select Visa Card and the Scotiabank Value Visa Card, which both offer 0% interest with a 1% fee for 10 months.

A balance transfer fee is a small bank fee charged up front to initialize the balance transfer. It is typically 1-3% of the balance transfer amount.

Reed Sutton

Latest posts by Reed Sutton (see all)

- byAir: The Ultimate Flight Tracker App? - Jun 12, 2026

- Review: TAP Air Portugal Business Class (A330-900neo) - Jun 3, 2026

- Scotia Momentum Visa Infinite+: Earn $300 Cash Back & $150 FlyerFunds - Jun 2, 2026

- Earn Cash Back Rebates on RBC Bank Accounts - Jun 2, 2026

- BMO VIPorter World Elite: Earn 70,000 VIPorter Points & $125 FlyerFunds - May 16, 2026