Meeting minimum spending requirements is one of the hardest points when it comes to earning a significant amount of miles and points to reduce the cost of your next vacation.

If you are interested in the cards that offer serious welcome bonuses, they often have minimum spending requirements of up to $10,000 or $15,000 in three months. This seems astronomical for the average person, who may at most spend a few thousand dollars per month. What about if you could generate spending on your credit cards without spending any actual money? Enter: the concept of manufactured spending.

Let’s take a look at the basics of manufactured spending and why you might consider implementing some of these strategies to take your travel hacking to the next level.

What is Manufactured Spending?

Manufactured spending is the process by which we can generate credit card spending without actually spending our money. These methods are often fee-free or have minimal fees associated with them.

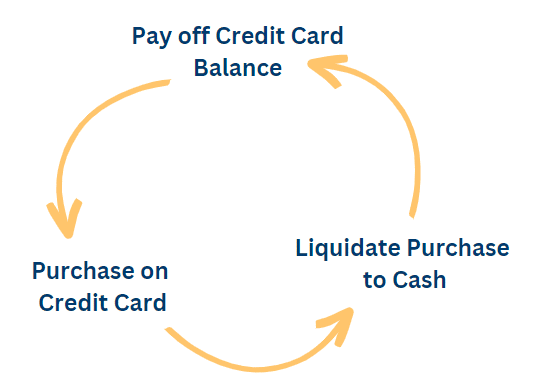

How this works is that we will make a purchase, liquidate that purchase into cash, and then pay off our credit card balance. From there, we can start the manufactured spending loop over again.

This loop gives us the opportunity to put spend on the credit card of our choice, earn the points or miles, and pay off the balance all free of charge. This means that we can generate a significant amount of miles without actually needing to purchase thousands of dollars in merchandise or services.

These methods also present a very easy way to meet minimum spending requirements on credit card welcome bonuses. Credit cards that have significantly higher spending requirements, that may have previously felt out of reach, are much more achievable thanks to manufactured spending.

Best Practices for Manufactured Spending

If you are going to engage with manufactured spending techniques, there are a few best practices you should keep in mind.

The most important tip is to practice good risk management, as we will touch on below. This means do not risk more than what you are willing to lose. For example, if you are manufacturing spend with physical merchandise; how are you going to feel if your liquidation method is no longer possible? This can be very scary and incite panic in many, especially when dealing with large sums of money.

I highly recommend mixing organic spending with manufactured spending on the credit card of your choice. This makes it look more legitimate, and is simply not a long list of transactions with the same vendor for the same dollar amount, which may arouse suspicion.

With any method, try not to get too greedy. While this is one area that I struggle with (who wouldn’t want to print EVEN MORE points?), it is important to keep manufactured spending methods sustainable. I’d rather earn 100,000 points a month for a full year, versus 150,000 points for three months, and then the method gets shut down due to extensive abuse. Sustainability is key.

Finally, if you do find a new manufactured spending method, ensure you are sharing with only those who you completely trust. Broader awareness and use of methods can contribute to them being nerfed or shut down, so keeping these in a close circle of colleagues is very important.

The Risks Associated with Manufactured Spending

While manufactured spending is absolutely attractive when it comes to an easy way to meet, it is not without risk. Manufactured spending, at its core, should always be an exercise in good risk management.

When you are looping credit card spend, roadblocks can happen at any point in the process. For example, your liquidation method suddenly may no longer be possible and you could be stuck holding the bag with merchandise or cash equivalent products.

As an example, I was running multiple PayPower cards and had my accounts locked. This took around two months to get People’s Trust to cut me a cheque so I could retrieve my locked money, deposit it into my bank account, and pay off my credit card balance. While I had the money to pay off the credit card balance while I was working through resolving this with People’s Trust, others may not have been so lucky and may have had to float a significant balance without proper planning and risk management.

My biggest piece of advice when it comes to manufactured spending is that you need to determine your own risk level, and have a plan in place should something go sideways. Depending on the method, you should always be able to get your money back, it may take time and a lot of frustration in dealing with certain companies.

How Can I Manufacture Spend?

Manufactured spending opportunities are one of the most tightly held secrets in the travel hacking and credit card rewards scene. If someone stumbles upon an opportunity that allows them to essentially generate an endless amount of airline, hotel, or credit card points, it makes complete sense why they wouldn’t want to share that with others.

There are a few publicly available manufactured spending opportunities that we have covered on Frugal Flyer:

These methods are covered extensively on public forums and other travel blogs, to the point where these methods would be considered public knowledge. While they may not be heavy volume (at least on the surface), they can be great tools in meeting your minimum spending requirements and put you on the track to earning more welcome bonuses.

We have also written about a few methods that worked in the past:

- Post Mortem: Revolut’s Revolving Doors of Remittance

- Post Mortem: Printing Bitcoin Cashback and Saving the Rainforest with the Mogo Prepaid Card

While these methods no longer work, they can provide some insight into previously available manufactured spending opportunities and what you should be looking for when it comes to new opportunities.

At the end of the day, the best way to learn about current manufactured spending methods is to network with other travel hackers. Most often, this takes the form of in-person meetups and continuing the conversation on Discord or other chatting apps. That being said, don’t ever be the person who just straight up asks for methods; it won’t give you the result you are looking for.

Best Credit Cards for Manufactured Spending

The best credit card for manufactured spending will always depend on the manufactured spending opportunities available to you.

For example, if the manufactured spending opportunity is available at a grocery store, you would want to use a card that offers 5x points or 5% cash back on grocery purchases. Similarly, if the opportunity was at a gas station, you would want a card that gives you the best return on gas station purchases.

Additionally, it always helps to have a few cards to rotate through. When manufacturing spend, you don’t want to draw attention from one specific financial institution. By holding multiple credit cards that offer 5x points on grocery purchases, you can more easily spread the manufactured spending around.

If you have a manufactured spending method in mind and are looking to apply for a new card, consider checking out the FlyerFunds Rebate program to earn cash back when you are approved for your new card.

Conclusion

Manufactured spending can be completely worth it if you find a good opportunity. However, it is not without its risks, and you should always be prepared to have to float the money should something happen during the manufactured spending or liquidation cycle.

Matt Astro

Latest posts by Matt Astro (see all)

- American Express (US) & No Lifetime Language (NLL) Offers - Feb 5, 2024

- Top Travel Hacks from the Obnoxious Autobiography of Justin Ross Lee - Jan 5, 2023

- Post Mortem: Revolut’s Revolving Doors of Remittance - Jun 23, 2022

- Review: Vought Rewards Black Card - May 8, 2022

- Manufactured Spending with the Reloadable Prepaid PayPower Mastercard - Jan 6, 2022

Can’t see comments