If you’ve found yourself on the topic of this post, you might have some suspicion that there is more to credit cards than meets the eye. Perhaps you’re considering signing up for one or have been getting offers in the mail, but don’t know where to start. Or perhaps you already have one (or more) but aren’t sure if you’re using them to their fullest potential.

One of the key credit card benefits we’re going to talk about at Frugal Flyer is travel rewards. Even if travel isn’t your thing, we’re going to show you that credit cards are useful for more than just travel rewards, as long as you just have the desire to get rewarded for spending money you’d have to spend anyways.

At Frugal Flyer, we don’t specialize in financial jargon or using blogging as a front for flexing (showing off) our status. Rather, we use simple English for the average person to understand how they can better their financial situation and take advantage of opportunities to travel on the cheap.

Let’s face it, not a lot of us have a lot of vacation time or enough money to go the places we’ve always dreamed of – and definitely not in business or first class. But for those of us with prudent financial habits, and decent credit history, the credit card game opens the door to racking up insane numbers of miles and points, and finding little cracks in the system we can use to improve our quality of life and go on those dream vacations or getaways we’ve always wanted.

But before we begin, we have to address a fundamental question that the financial institutions, school systems, and government have essentially failed to explain to Canadians in any adequate measure: how the hell do credit cards even work?

Before we get started with recommending credit cards, we need to give you the tools to understand how revolving credit works so that you can rack up the points or cashback necessary to achieve your goals.

If you think this is for you, it’s of the utmost importance that you pay attention to what you’re about to learn. That isn’t me being clickbait-y or trying to bamboozle you, it’s telling you the truth so that you turn credit cards into a way to enhance your life to do things like go to Disney World for free rather than fall into a spiral of debt or missed credit card payments.

This post is long and comprehensive, but when you’re done, you should have an idea of how to step into the credit card rewards game.

Step 1: What is Revolving Credit and Compound Interest?

According to the Financial Post, the average Canadian owes $4,240 in credit card debt, and yet most Canadians have little to no idea how credit cards work, despite receiving legally-mandated disclaimers of “fine print” that explain how charges and fees function

So let’s translate a few terms from “finance-ese” into a language we can understand.

A credit card is a form of revolving credit. That means that when you are issued a credit card, it has a limit that you are allowed to spend up to, and you are able to use any unused portion of that credit limit when you want (essentially borrowing the money). Because that credit is available to you constantly but isn’t always completely used up, it revolves, as opposed to a fixed form of credit such as a loan where you’re given a lump sum or a good like a vehicle and obligated to pay over time.

Now, that doesn’t mean you should spend outside your means. Indeed, the banks make a lot of money when they offer you, say, $5,000 and you spend that money without having it in the bank to pay off your card.

This leads to what is known as interest, and it’s a key part of understanding how credit card billing works. When you make a charge and it appears on your credit card account, it is added to that month’s statement. The statement will always be issued on or around one day of the month, and you’ll have until a certain date to make a minimum payment – this is the amount you must pay in order to keep your account current and not get in any trouble with your credit scores (more on this later).

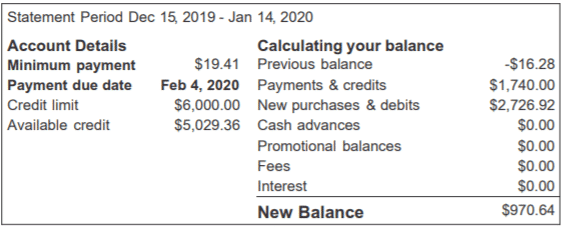

Let’s look at an example:

This is my statement from Roger’s Bank of Canada (who, coincidentally, issue a good cashback card that has been subject to recent and unfortunate devaluation). The screenshot has all of the relevant information: it shows my credit limit, the amount of credit I have left, the amount of spending I’ve done this month, the fees or interest I’ve been charged, and the minimum payment.

What this means is that I had to pay at least $19.41 by February 4th or else have a late payment issued on my credit report. Fortunately, because this is Canada, I will not pay any interest at all until the 4th – this is what is known as a grace period, or a time when no interest will be charged on any of my transactions.

However, if all I had paid would have been $19.41, then I’d be charged a whopping 19.99% annual interest rate (AIR) on the remaining $956.23 for every day past the 4th that the balance remains unpaid. If I were to continue making the minimum payment, it would cost me over $930 in interest and take me 10 years and 8 months. Ouch!

Why would I have to pay almost as much in interest charges as I do on the base rate? Well, it’s a magic little thing called compounding interest. I’ll give you a more detailed explanation, but for the most part, it works thusly:

Compound interest when it comes to debt is a serious issue. It’s what causes so many Canadians to carry debt over time, and it’s because it allows lenders to continue charging interest on unpaid interest, thus making you owe more money over time. All payday lenders work this way, and TD Bank recently transitioned to charging compound interest on its credit cards.

Some credit card issuers, such as Scotiabank, RBC, and CIBC do not charge compounding interest, only simple interest, wherein they charge you interest on the unpaid balance of goods you’ve purchased, but let’s be real here – do you want to be paying a 20% markup on anything?

I’d like to share a graph I’ve made that took me countless man-hours and involved the crunching of enormous quantities of data to explain exactly how compounding interest will work over a period of time:

This is why at Frugal Flyer we always recommend paying your bills on time and in full.

But there’s a silver lining: remember that grace period we mentioned? It means you won’t be charged interest until the minimum payment date has passed. This means that it can actually be a big bonus to your cash flow: if you pay something on the 5th of the month but your statement doesn’t cut until the 31st, you’ll have that 21-day interest-free grace period starting on the 31st. So you won’t be paying interest for a total of 47 days!

Just make sure to pay it off in full, otherwise, you fall into the trap detailed above.

Let’s also take a moment to explain the kinds of transactions out there so you have an idea:

Types of Transactions

Purchases: This is the most common type of purchase. You’ll buy something on your credit card, the charge will enter a “pending status” (wherein the payment network is transferring funds to the merchant), and then a few days later it will be “posted” to your account and be ready to show up on your next statement.

Cash Advances: This is a transaction where you charge your credit card so you can withdraw actual hard cash. We at Frugal Flyer strongly discourage this because it never counts against the minimum spend of a credit card and is always subject to additional fees and punitive rates of interest. So short of being trapped by a mustache-twirling villain in Turkmenistan and needing hard cash to jerry-rig your black market Iron Man suit to escape, don’t do it, OK?

Also be advised certain types of “cash-like” transactions will sometimes incur cash advance fees depending on the credit card issuer (I’m looking at you, lottery tickets).

Balance Transfers: This is a type of transaction where the credit card balance of one card is transferred to another card, usually at a lower rate. For example, MBNA is a card issuer that often offers very competitive low-rate balance transfers. For example, in one of their recent offers, you would pay 0% interest for 10 months in exchange for a transfer fee of 1% of the total amount transferred (eg: $50 for a $5000 transfer), and your interest would revert to the regular 12.9% on that card at the end of the 10 month period.

Note: Never under any circumstances whatsoever and we mean whatsoever make any kind of transactions or spend on a credit card with a balance transfer, period. This is because you will fall into the system known as “proportional payoff” wherein you’re going to be paying interest in some quantity no matter what until the entire credit card balance is paid off.

Related: Balance Transfers: How to Leverage Low Interest Debt to Earn ‘Free’ Money

Hope you’re still with us. If this info has clobbered you, we hope you’re OK. But now that you understand the basics of interest, minimum payments, and transactions, you’re equipped to start learning how and why issuers extend credit, and how you can use that to up your travel game and quality of life.

Step 2: How Algorithms Determine Your Creditworthiness

In Canada, the companies Transunion (TU) and Equifax (EQ) provide credit monitoring services that determine how creditworthy individuals are. This means that they’re responsible for collecting data on how you utilize your credit products and issuing that information to lenders so they can decide if you should be given a car loan, mortgage, line of credit, or new credit card. Having and retaining good credit is imperative within this hobby.

Learn More: Credit Scores: Everything You Need to Know

According to Equifax, one of the two main credit bureaus, a credit score is calculated by looking at many aspects of your credit history and by using an algorithm. Through this calculation, Equifax’s algorithm spits out a final value between 300 (Supernaturally Bad) and 900 (the Credit Messiah).

The other issuer, Transunion, has a slightly different algorithm to calculate your final score but the basics of what is fed into it remain the same:

Payment History: 35%

This is the most important part of your score, and it measures how often you’ve made payments per the rules of payment dates we detailed in Step One. Always making your minimum payment listed on your credit card statement, and preferably paying your balance in full, will be very beneficial to your credit score and allow you to conduct the credit card and travel game effectively.

Utilization of Credit: 30%

Credit Utilization is something that not many people are taught about. What this means is that each month, your outstanding balances will be reported to the credit bureaus. If you have, say, $300 in balance on a card with a $1,000 credit limit, and that’s your only credit product, then your utilization is 30%. If however you have a $4,000 credit limit on one card but possess 5 cards with $10,000 limits, your utilization is only 12.5%, so typically your score will be higher.

At the same time, to add extra confusion to the system, the individual balances on cards in proportion to their individual credit card limits can also cause significant adjustments to the score, so even if you have a total of $100,000 in credit but one card with a $2,000 credit limit has $1,900 in balance on it, this could adversely affect your score. Aren’t algorithms fun?

Credit History: 15%

This is a calculation of the average age of all your accounts. Had a card for 10 years? In general, you shouldn’t close it as it’s helping your entire age of credit history. At the same time, sometimes even closed accounts can contribute to your overall history, so as long as your financial habits are good and you’re paying your balances and never being late this is generally fine. The younger your history, the less likely you are to be approved. For example, the credit card company MBNA won’t approve applicants with fewer than 2 years of credit history.

Public Records: 10%

Public records relate to if you’ve had any kind of bankruptcies or major delinquencies such as a consumer proposal in the past. If you’ve had one within the past 7 years, most issuers won’t issue you credit due to the riskiness associated with your credit file.

Inquiries: 10%

When it comes to applying for new credit, there are two methods of accessing credit that lenders and underwriters will use. The first kind is a “hard pull” (HP) where the assessor will add your inquiry to your credit report, noting the date, which is then visible to any other assessors. A hard pull will cause your overall credit score to dip a few points (anywhere from just a few points, all the way up to fifty, depending on the richness of your overall profile).

It also means that if you have too many of these hard pulls, you may be declined for more products as you’ve been engaging in what the underwriters consider ‘credit-seeking’ behavior. If that happens, it’s usually a good idea to back off for a while.

The second type of pull is a “soft pull” (SP) where the issuer doesn’t add the inquiry to your credit file and chooses to approve or decline anyways.

All of this information will help you generate a three-digit score that issuers will pull from, and at Frugal Flyer we recommend you sign up to monitor your score at ClearScore Canada or Credit Karma Canada for Transunion credit bureau information and Borrowell Canada for Equifax credit bureau information.

Related: Borrowell vs Credit Karma: Which Is Best?

However, be advised that it’s not just your score that issuers will assess: they’ll make decisions also based on your income and how much total credit you have available. Some issuers, such as RBC, have a cap of total credit before they’ll issue you more, whereas others such as American Express are known to be super lenient.

The following is a non-exhaustive list of which banks pull from which credit bureau:

Transunion

- American Express

- Canadian Tire Financial Services (CTFS)

- MBNA

- Royal Bank of Canada (RBC)

- Roger’s Bank

- Scotiabank

- Tangerine

Equifax

- Bank of Montreal (BMO)

- Capital One

- Canadian Imperial Bank of Commerce (CIBC)

- Desjardins (And most Credit Unions that operate on the Desjardins network)

- National Bank of Canada

- Toronto Dominion Bank (TD)

- Simplii Financial

Both

- PC Financial

Step 3: Understanding Payment Networks

So now we have an idea of how credit cards are actually billed and how your credit score works. So what? What else do we need to understand before we go and start applying for cards to rack up those bonuses and points?

In Canada, credit card transactions are dominated by three major networks: American Express, Visa, and MasterCard.

These networks make money by charging what are known as interchange fees, where merchants have to pay the credit card networks certain fees on each transaction in exchange for accepting their cards in-store. These fees are how companies pay out their rewards programs to customers like us who want to maximize our travel and points game.

Within Canada, American Express tends to give the best rewards, but they also charge high fees so not every merchant accepts them. Conversely, Visa and MasterCard are accepted much more widely but tend to not provide benefits as generous as those of Amex. However, each network issues different levels of cards, from very basic cards to premium cards. These differ because the more basic cards charge merchants lower interchange fees, but the more premium ones charge higher fees while rewarding cardholders with much better rewards.

American Express is also a bit of a unicorn because it is the only issuer in Canada that issues a special category called charge cards. These are cards that must be paid in full after their statement date – you cannot carry a balance. Their charge cards, such as the Platinum, are also usually the providers of their most lucrative awards and benefits such as free lounge access.

Learn More: Charge Cards vs Credit Card Differences

This means that merchants successfully lobbied Parliament to reduce the number of premium cards by adding clause 9 to the Canadian Code of Conduct around credit cards which states: “premium payment cards shall only be given to a well-defined class of cardholders based on individual spending, assets under management, and/or income thresholds.”

This means that in Canada, the highest tiers of credit cards are often subject to minimum income requirements. For MasterCard, their highest tier is their World Elite cards, which have a requirement of $80k individual salary or $150k household income.

For Visa, their Visa Infinite tier requires $60,000 individual income or $100,000 household income. American Express tends to have no published income restrictions on their cards aside from a requirement for high annual fees which tends to dissuade lower-income individuals.

What this means is that to really maximize your points game, you either have to make a large amount, or have an alternate route to gaining the best cards out there. Please be advised I’m only engaging in speculation and do not condone lying on applications.

However, we do know anecdotally that lenders often don’t verify the income stated on applications. In addition, household income can be any loved ones living with you and their income also cannot really be verified, so make of that what you will. For younger readers, this does usually count your parents. For married folks or those running small/side businesses, remember that your spouse or revenues from a business can also count.

Also, note that you are in no way obligated to hold cards only with your primary financial institution, you can hold them with any credit card company so long as you meet the credit and income requirements.

Step 4: How Do Credit Card Rewards Work?

So, now we know how credit cards work, have an idea of how credit scores work, and know which payment networks operate in Canada, as well as what they require of cardholders. The next question is: how do we go on that dream vacation, or even just visit family on Christmas with our miles and points?

Read: Beginner’s Guide to Miles & Points

To answer this question, we must understand what we are looking for. There are three major redemption options in Canada for credit card rewards: cashback, merchandise, and travel.

Across the board, no matter the miles and points loyalty program, redeeming points of any kind for merchandise is almost always a terrible idea that will cause you to spend points at a ridiculously low rate.

Cashback can be a great option, heck, I hold the Roger’s World Elite, but it isn’t really the focus of the Canadian credit card scene since there are so many better options when it comes to earning credit card rewards.

That brings us to travel, which given the name of the blog, you can probably guess is our main purpose. There are going to be several programs that we discuss, but before we do, let’s address the elephant in the room: signup/welcome bonuses and daily spending.

The best way to accumulate large numbers of any kind of points will be to earn rewards from the signup bonus. This is an offer a bank will give to customers who open a new credit card and hit a minimum spend within a given amount of time; usually 3 months. They’ll then reward you with a very large number of points as soon as you’ve hit the spend. This means as somebody new to the credit card game, to gain lots of points, you’ll probably be opening a variety of credit cards, but we’ll get to that in the next step.

So, what programs are available to Canadians? I personally classify them into four categories: American Express Membership Rewards, Airline Rewards, Hotel Rewards, and bank-issued rewards (or in other words, the rewards points specific to individual banks).

American Express Membership Rewards (MR)

The main reason I categorize Amex rewards as their own thing is because of how easy they are to acquire and change. Cards like the American Express Platinum card often have a high welcome bonus, which can then be transferred at a 1:1 ratio to the Aeroplan or British Airways Avios airline programs, transferred to the Marriott Bonvoy program at 1 MR:1.2 Bonvoy, or redeemed at a value of 1 cent per points (CPP) against any travel expenditures. The sheer interchangeability of Amex MR makes them super useful.

Airline Rewards

At Frugal Flyer, we’re going to be writing in-depth analyses of all the major airline reward programs so stay tuned. But here’s a short summary of the options that are available to Canadians:

Aeroplan: Aeroplan is the rewards program owned by Air Canada that most Canadians can start to rack up in large quantities. The reason it’s so useful isn’t just its availability or use on Air Canada, but the fact that it can be redeemed at great rates on the Star Alliance network of airlines, though the redemption will be changing in Q3 of 2020. Of all the programs detailed on Frugal Flyer, this one receives the most attention, so don’t change that dial.

Avios: Avios is the rewards program of British Airways, but the reason it’s so useful to Canadians is that it can be used in conjunction with the OneWorld alliance, and it can be acquired by transfers from American Express Membership Rewards points or RBC Avion Rewards Points. As always, we’ll be writing detailed posts to maximize this.

Hotel Rewards

While there are many hotel programs around the world, in Canada the only program that Canadians can readily get many points in is the Marriott Bonvoy program, which has been subjected to several devaluations, spawning the verb “bonvoyed.” At the same time, we will be writing about it extensively as it is easy to stay at exotic properties like the Ritz Carlton by getting the American Express Bonvoy Personal and Business cards.

There is also the Hilton Honors program, but it isn’t easy to get points as a Canadian without entering the American credit card market, which is possible but beyond the scope of this post.

We will also be covering a few of the less well-traveled loyalty programs out there, or at least address them, so remember that just because your preferred hotel loyalty program isn’t listed doesn’t mean it holds no value.

Bank Issued Rewards

All of the big banks in Canada issue credit cards that offer rewards in the form of a proprietary internal currency, for example, Scene+, or BMO Rewards. These have to be used internally within the portals or banking systems of the issuers themselves, and can’t be transferred outside the lender’s ecosystem.

This can be particularly harsh when subjected to arbitrary devaluation – can you imagine faithfully collecting huge quantities of points only for them to be devalued? No fun at all. Of course, it’s not just bank monopoly money that’s subject to devaluations; points programs including airlines and hotel rewards can also be devalued.

So while we won’t state that there is no use getting the funny money issued by certain bank credit cards, and we will be covering how to use those points in the future, be advised that they aren’t always the best option out there, especially if you’d rather be hitting minimum spends on other, better cards that reward you in regular airline points or transferable points such as Amex Membership Rewards.

Step 5: Learning to Earn Credit Card Rewards

So remember how we stated earlier that the best option to earn large quantities of miles and points was by hitting the minimum spend requirement (MSR) on a welcome bonus? Well, buckle up, because we’re about to go to butter country. If you’re afraid of fat, don’t come for the ride.

The level of aggression that varies between individuals, and signing up for new rewards credit cards should always be based on your individual ability to pay your bills in full every month as well as the feasibility of achieving the sign-up bonus. Don’t sign up for a card if there’s any doubt in your mind that you can get the bonus, as then you’re just wasting a hard pull on your credit score.

But wait, you ask, won’t this hurt my credit score? Well, remember, when we went through the credit score section, your inquiries only make up about 10% of your overall score. What matters far more is the length of your credit history, making all your payments on time and in full, and not having a crazy utilization ratio.

Try to stay beneath 30% of all overall credit showing on your statements and you should be fine. In fact, if you start with only a single credit card with a low limit, adding more cards can actually improve your score by improving your individual and aggregate utilization ratios. On the other hand, if you’re ever declined due to too many inquiries, either switch credit bureaus or back off a little.

Now, let’s get back to the question of how aggressive this can be: some people will want to do 15-20 cards a year, while for others, maybe only 4-5 cards a year are what you can achieve or are comfortable with.

Also, be aware that here in Canada we are relatively blessed: most issuers haven’t cracked down too heavily on repeated welcome bonuses, which means that with many cards you can get a card, hit the bonus, hold it for a few months, cancel the credit card, and then reapply and get the bonus a second time.

The general rule of thumb is to hold the credit card for six months, cancel the card, and wait for six months before re-applying. Be advised that, when it comes to American Express, they’ve fixed their backend IT to prevent this from occurring on most of their personal cards. If you run a business or have a serial entrepreneur spirit, then perhaps you’ll have better luck with the signups. Again, don’t do anything past what you’re comfortable with but if, for example, you are trying to get lots of Aeroplan points you can focus on the Aeroplan-branded cards from TD and CIBC and not have to worry as much about other issuers.

When it comes to credit card rewards, always remember: fortune favors the bold.

Step 6: So What Card Should I Get?

Before we even make recommendations, Frugal Flyer invites you to use the information above to empower yourself. What are your goals? What do you want? We focus on travel, but do you want cashback? Cool, adjust your strategy, or drop us a line and see if we can help. Do you just want a flight or two a year? Or maybe you’re trying to go to a resort in the Maldives? There’s no one-size-fits-all solution to everything, but your game plan can be adapted to your own income and financial situation if you’re willing to keep on learning.

Aside from that, what I will say before taking off is that, when in doubt, try to accumulate either Amex MR points or Aeroplan, as these are probably the “most valuable” and easiest-to-use points available to Canadian consumers. As you are diving into the Canadian credit card scene, always remember to never do anything you’re super uncomfortable with – unless you’ve done your research and are OK with taking a calculated risk. After all, no risk, no reward.

Conclusion

Credit cards are a strong financial that can be utilized for your benefit but it is important to understand the ins and outs so you don’t get yourself in a sticky situation. Before you sign up for your first credit card, learn more about why you should consider using a credit card as part of your personal finance habits.

While we are able to take advantage of many of the benefits such as welcome bonuses and perks through credit cards as part of our miles and points hobby, the value of these can easily be wiped out if you end up paying interest charges and carrying debt.

Reed Sutton

Latest posts by Reed Sutton (see all)

- byAir: The Ultimate Flight Tracker App? - Jun 12, 2026

- Review: TAP Air Portugal Business Class (A330-900neo) - Jun 3, 2026

- Scotia Momentum Visa Infinite+: Earn $300 Cash Back & $150 FlyerFunds - Jun 2, 2026

- Earn Cash Back Rebates on RBC Bank Accounts - Jun 2, 2026

- BMO VIPorter World Elite: Earn 70,000 VIPorter Points & $125 FlyerFunds - May 16, 2026

1 comment on “How Do Credit Cards Work?”