Part of maximizing rewards from credit card spending is focused on being approved for your next credit card. After all, the best everyday multipliers on many credit cards are 5x or 6x points per dollar spent on specific categories. On the other hand, some credit card welcome bonuses work out to an earning rate of 50x points per dollar on all purchases since they award a massive chunk of points for a nominal amount of spend.

In order to take advantage of every opportunity available to you with credit cards, you need to understand the credit score system to determine your eligibility for obtaining additional credit, and in turn, your next credit card. Not to mention, credit scores are an integral part of overall financial health, as they will be looked at any time you are applying for credit outside of just credit cards, including for personal loans and mortgages.

Let’s take a look at everything you need to know about credit scores to not only understand how a credit score is calculated but also what they mean for your financial health.

What are Credit Scores?

Your credit score is a snapshot of your financial picture, but it’s not a black-and-white tool that will guarantee you approval for a new credit product. With that disclosure, your credit score is one of the only things you can use as a consumer to judge how the banks view your trustworthiness and the likelihood that you will be approved for additional credit.

Ultimately, credit scores are born the moment that you begin to borrow money from a financial institution, whether that be for a credit card or a personal loan (like a car loan or line of credit). Think of credit scores as a measuring stick for how reliable you are when obtaining and paying back any sort of credit product. Credit scores follow you around your whole life which is why they are important to build and maintain over a long period of time.

Every time you apply for a new credit product, the bank or institution will check your credit score. This is commonly called a “hard pull” but it doesn’t impact your score the way most people think. Below I’ll explain the factors that play into credit scores and how to keep your score above average.

The Components of a Credit Score

Back to the point (lousy pun, I’m sorry) of this article, in order to manage your credit score and increase your chances of being approved for *almost* every credit card you are interested in, you need to understand the components of a credit score and how they are weighted and in turn, how your actions affect your score.

Payment History – 35% of Credit Score

The most important thing a bank will want to know is if you pay your bills on time. While paying your bill in full every month is strongly recommended, that’s not what payment history refers to. Payment history is considered perfect if you’ve paid your minimum payment by the due date.

So, if you can’t pay your balance in full for one month, your payment history will remain perfect as long as the minimum payment is received roughly two weeks after your statement posts. Your statement will tell you exactly when your minimum payment is due.

Credit Utilization – 30% of Credit Score

How much of your available credit you’re using, or credit utilization, is almost as important as your payment history. Credit utilization is often the least known factor among most consumers and understanding and taking advantage of this factor can dramatically improve your score.

Credit utilization is the percentage of credit being utilized when compared to the total amount of credit that has been extended to you. Credit utilization is only calculated when the statement posts, meaning that the only number that is recorded is the balance on your statement. The reason why credit utilization is so important is that it (kind of) shows how responsible you are with spending.

The theory behind this is that if the banks give you a $1,000 credit limit, that’s the maximum amount of credit risk they are willing to extend to you, based on your application factors such as income and existing credit score. If you’re spending $900 (or 90% of $1,000) every month, in theory, you’re maxing out your finances and are considered a greater liability to default.

For some consumers that only use one credit card, opening a second one may increase your score in the short to medium term. For example, if you now hold two credit cards each with a $1,000 limit, and are still spending $900 per month, you are now only using 45% of your available credit rather than 90%. Lowering your credit utilization will usually equal a higher score.

The flip side of this is that banks may give a tiny credit limit when you first apply, depending on their risk appetite, and slowly increase it as you pay your bill on time. What this means is if you’re approved for a $5,000 credit limit and spend $3,000 each of the first three months to hit a $7,000 minimum spending requirement, your credit score may go down if your statement is posting with a $3,000 outstanding balance. This happens because you’re showing “risky” behavior by using 60% of your credit limit.

The next logical question is: How can I build a better relationship with the bank and be viewed as a less risky customer?

Ideally, banks want you to use 20% or less of your available credit. You might then ask… “So Daniel, with a credit limit of $5,000, I can only spend $1,000 a month?! I’ll never hit the $7,000 minimum spending requirement!”

Please do not fret, young Padawan. I have a solution for you. All you need to do is pay off your balance to 20% of your available credit before your statement posts. You may wonder, shouldn’t I pay off the whole thing before the statement is posted? Surprisingly, no.

You need to actually borrow money to show that you can borrow money responsibly. If you have a credit card statement posted with a $0 balance, it’s like you never borrowed anything, as the actual “borrowing” period is two weeks after your statement posts. That is commonly referred to as the interest-free grace period. Leaving a small balance to post on your statement and then paying it off shortly thereafter is oftentimes the best play to build your credit score.

Length of Credit History – 15% of Credit Score

How long you’ve been borrowing money is important, but it won’t save you if you don’t focus on payment history and credit utilization. So, while it’s great to start a credit profile when you’re young, it’s more important not to make mistakes with payment history or utilization.

This is important for any readers that have adult children. While it can be tempting to get a 15,000 Membership Rewards point bonus through a credit card referral to an American Express Cobalt card, it could be a downward spiral. If you’re not confident in their ability to manage spending, I recommend adding them as an authorized user to one of your cards first to see how their spending habits relate to their income.

Length of history will also come into play when reviewing your current credit card lineup. As you add high-value cards to your wallet, maybe you have an older credit card that hasn’t been touched in months or even years, and you consider canceling it. This would be a big mistake.

By canceling one of your oldest credit cards, you also cancel all of the outstanding payment history that is associated with that card, dropping your score. I made this mistake myself when I canceled my oldest TD Green credit card, which I thought I didn’t need as it offered zero rewards. Not only did I limit myself by removing an option for a future TD Product Switch, but I noticed a drop in my score the next month.

Rather than canceling, you can usually switch a card to a no-annual-fee option and preserve the credit history. To keep the card active, I have reminders set to use the cards twice per year for an Amazon balance re-load of $5. I also set auto payments for these cards so I don’t forget to pay the bill.

New Credit Applications – 10% of Credit Score

The most common question I get when I tell people I have 10+ credit cards is, “How is your credit score not ruined?”. And that’s because new credit inquiries don’t affect your score in the long term. While your credit score may have a slight dip every time you ask a financial institution for an additional credit product or credit limit, it will recover within a month or two. This is called a “hard check” and doesn’t have any long-term lasting impacts.

After becoming comfortable with your ability to hit the minimum spending requirement on new credit cards, the best strategy is to apply for a couple of cards in quick succession and then take a break for 3-4 months. This will allow your score to recover, hit your minimum spend(s), and then rinse and repeat.

If you notice a significant drop in your score, check to confirm that your utilization wasn’t abnormally high and that you’ve made all your payments on time.

Credit Types – 10% of Credit Score

The final and least impactful factor is the types of credit you have. This only becomes important if you’re chasing an 810+ credit score. Showing the banks that you can manage different types of credit, such as a mortgage, car loan, line of credit, credit card, etc., brings your financial picture into focus.

Let me put it this way, you won’t get declined for a TD Aeroplan Visa Infinite card if you’ve never had a car loan, but you may be asked for a few more years of T4s when applying for your first mortgage. I wouldn’t (and don’t) go out of my way to get a new loan to diversify my credit profile.

The Importance of Good Financial Habits

Rule number one when you dive into the world of miles and points is do not get into debt. While buying something you don’t need when chasing a sign-up bonus may be tempting, that is a slippery slope. The idea behind credit card rewards is that you would receive the points anyway on everyday purchases you need or intend to make. Similarly, if you are already carrying a debt load, this is probably not the right hobby for you at this point in time.

Read More: How to Build or Repair Your Credit Score in Canada

If you’re considering a card with a higher sign-up bonus than you’re comfortable with, see our guide on methods to hit a minimum spend requirement and ensure you have a plan before applying for the credit card. Or if you’re open to creative solutions, manufactured spending will be up your alley. While there is a steeper learning curve and you may pay some fees to reload your PayPower card or incur a small loss to drop ship an iPad to a buying group, it is way less expensive than paying interest.

The long and short of it is don’t get into debt if you are interested in entering the world of miles and points. If you don’t think you can manage your spending this will not be a profitable endeavor, and you should focus on establishing and maintaining good financial habits first and foremost.

How to Check Your Credit Score for Free

In Canada, we have two main credit bureaus that track all your financial history: TransUnion and Equifax. While you can pay them directly to check your credit, there are free services we’ve covered extensively that allow you to access your credit score and credit report at no cost to you.

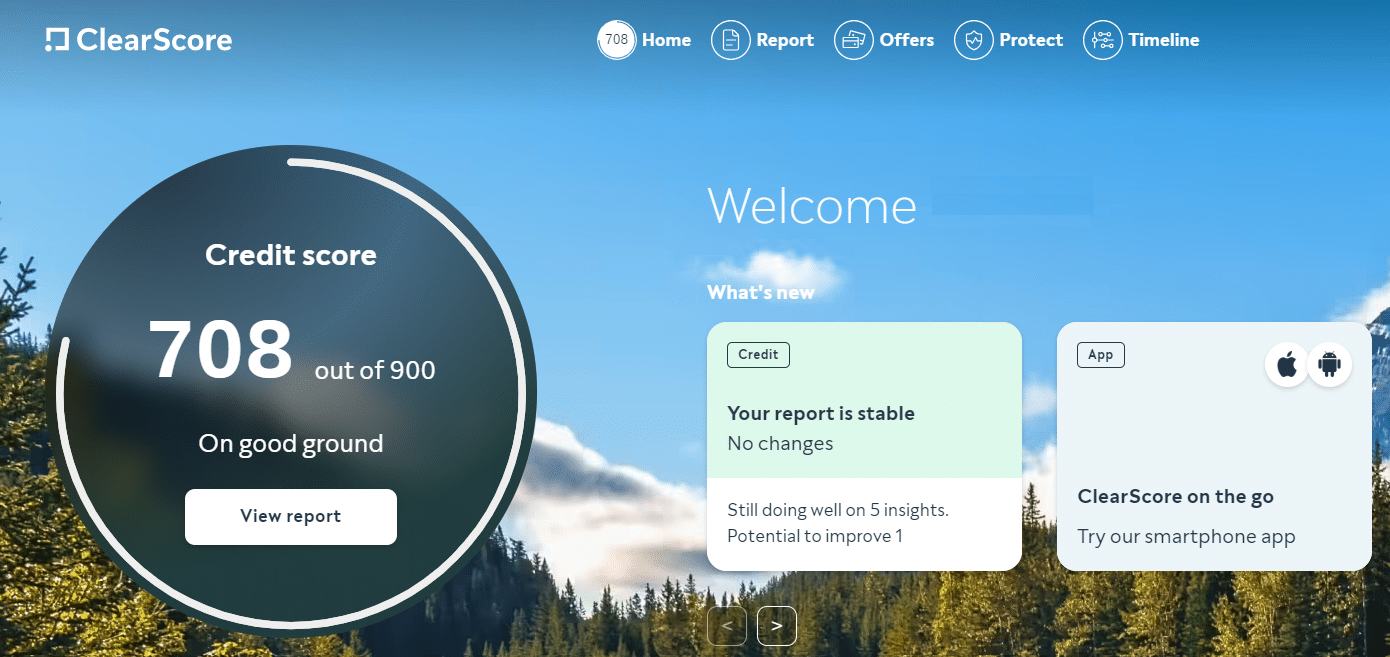

ClearScore Canada is our preferred free service to check your credit score and report, as they offer a quick sign-up process and an interactive dashboard to better understand your credit score. ClearScore goes even further than other services, as they also provide identity protection monitoring and credit report graphs, and other visualizations. ClearScore pulls from Transunion, so it should be paired with another service that pulls from Equifax so you can see how your credit is reported within both agencies.

You can sign up for ClearScore Canada here and get access to your credit score within three minutes.

Borrowell Canada is a free service that consumers can use to check their Equifax credit score and report. On the other hand, if you are looking for an alternative to ClearScore, Credit Karma Canada can be used by consumers to check their Transunion credit score and report for free.

If you’re curious as to the pros and cons of either service and if you should consider using both, check out more about Borrowell vs Credit Karma. Having an account at both can be a great way to have access to both scores so you can check the correct credit report that the lender will use when you apply for your next product.

Conclusion

Credit scores are a funny business and it can be difficult to understand them as a consumer. During my 5-year career in car sales, I saw some people who had excellent credit scores but didn’t deserve it, and some customers who never missed a payment but had a score south of 700.

While we may never know 100% about the algorithms that are used to determine credit scores, knowing the basics of what banks look at when they pull our reports allows us to manage our financial health, and in turn, our credit applications for maximum value.

Frequently Asked Questions

If your score exceeds 750, you should get approved for most cards that you apply to (unless you have excessive inquiries or other oddities that certain financial institutions take issue with).

The rule always has exceptions, but if you’re consistently north of that benchmark, you’re fine. There are some data points of American Express approving customers with a credit score of just above 700.

Utilization is the best way you can do this. Before you apply to any card, make sure you don’t have any balances close to your credit limit. Staying below 20% when your statement posts is the sweet spot.

It depends. If it’s your oldest card, yes, it will. If the card is a year old, only a minor effect or potentially no effect. You should hold a credit card for at least six months before closing it as a general practice to reduce the impact that closing a card will have on your credit score.

As an individual, you can check your credit score whenever you want, as much as you want, without impact as these are considered “soft credit checks”. Generally, your score will change every one to two weeks, so there’s no reason to check it any more than that.

Daniel Burkett

Latest posts by Daniel Burkett (see all)

- Rove Miles: Guide for Canadians - Jun 29, 2026

- Review: Westin Verasa Napa - Jun 24, 2026

- Review: JW Marriott Orlando Bonnet Creek Resort & Spa - Jun 17, 2026

- Wyndham Rewards Experiences: What You Need To Know - Jun 1, 2026

- Review: River Terrace Inn Napa - May 27, 2026