I’ve been in Miles & Point since 2019. One of the most common questions I’m asked by my fellow travel enthusiasts is whether I think it’s worth it to hold onto one of a plethora of high-end credit card products commanding hefty annual fees.

This question almost always comes after the first or second year of card membership in which the holder has already earned their welcome bonus and now wants to know if forking over a couple hundred dollars is worth the price of renewal. Or perhaps, there is a second-year welcome bonus component on the card.

Today, I want to leap into defining what I view as a premium credit card, and what features a premium credit card product should include, and then build a baseline for finding a valuation that such cards provide. Then it’s time to get into the math of determining whether a card is worth keeping around for another year.

What is a Premium Credit Card?

When I took my MBA, I was lackluster in the accounting courses. The lessons could be hard; the numbers doubly so. However, one thing that stuck with me from those courses was how to find valuation for goods and services, how to calculate it, and then how to turn this complex financial information into real-world decisions.

I want to do that with credit cards, so first we need to establish what a premium credit card is. While many Canadians would view any credit card that commands an annual fee as “premium”, the products to which I wish to refer today are the high-end products commanding large annual fees and often coming with a plethora of benefits.

Therefore, for me, a premium credit card is a product whose annual fee is $250 or higher, which has some form of travel benefits such as lounge access, airline status, travel credits, travel loyalty bonuses, or any combination of all the above. We’ll be working with this definition throughout this article.

For the purposes of this article, I also know that we’ll be measuring historical usage of benefits, rather than their future use. I know past usage isn’t a perfect gauge of the future, but it’s a decent measurement of the value you’re likely to get from your premium credit cards.

Please note I’m also not accounting for points you may be earning from daily purchases; this is because unless your volume is significantly massive or exclusively in multiplier categories, it’s probably not going to change your ability to travel or impact the quality of your travel.

Valuing Your Premium Credit Card: Full Retail Price

The first way we will establish a baseline for calculating the value that a premium credit card gives you is by using what I call the “bank method” or “marketing method.” This is the strategy employed by banks in their glossy brochures to entice you to sign up for one of their products by advertising an enormous dollar amount worth of benefits.

For the purpose of this method of calculation, we will use the full retail price of every benefit your card gives you as if you would be paying that product or service’s nominal retail price.

For example, let’s look at the Priority Pass Airport Lounge program in Canada, a benefit that is offered on several credit cards. Their basic membership tiers require an entry fee of $35 USD (approximately $48 CAD at the time of writing this article) to enter one of their lounges. Thus a credit card offering lounge entry via Priority Pass gives you $48 of value every time you enter a lounge.

Similarly, if your credit card, such as the American Express Business Platinum card, provides you with a status boost such as Marriott Bonvoy Gold status, and this membership results in you receiving room upgrades, then we calculate the value of that upgrade based on the retail price.

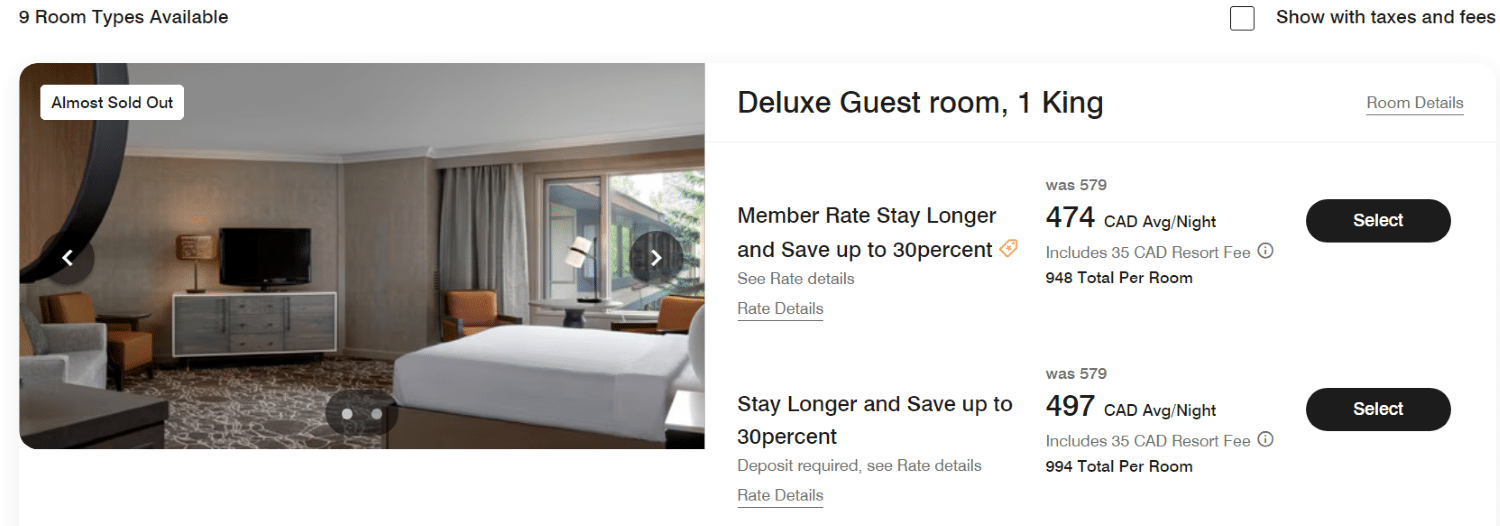

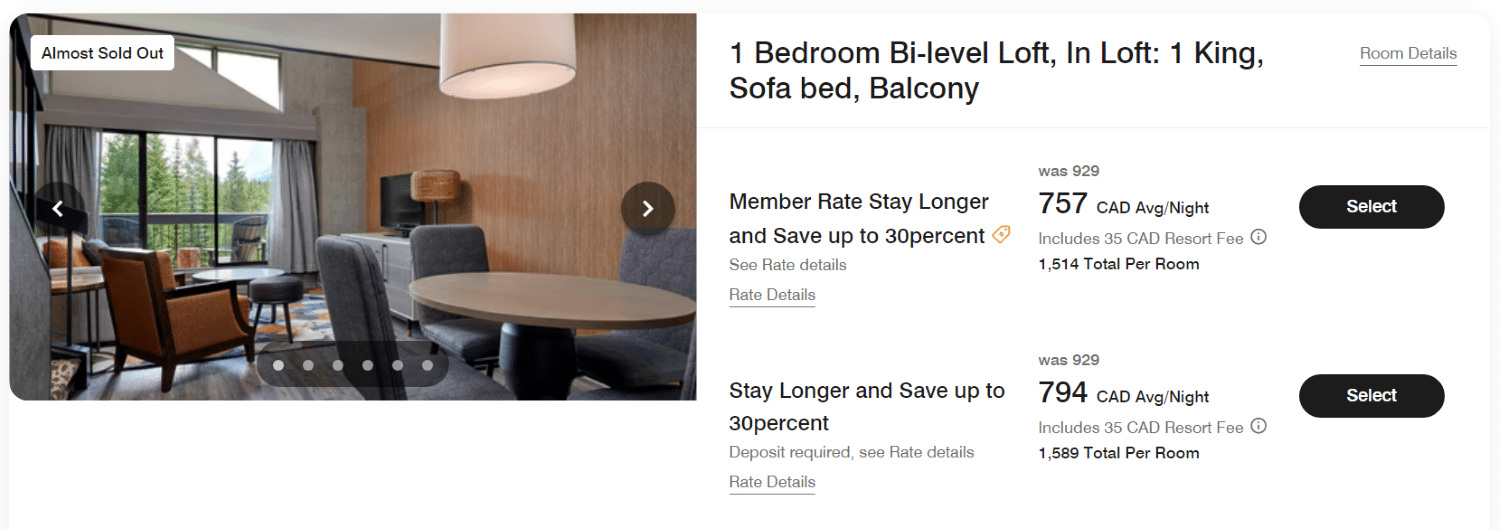

Let’s take a look at this room at my favorite property in Canada, the Kananaskis Mountain Lodge whose normal rate is $474 a night.

The nightly price of a suite on the other hand is $757.

Therefore, the value of this upgrade is a whopping $283. Not too shabby, eh?

With these prices in mind, let’s calculate a credit card’s benefits based on this formula at year’s end. For example, we can use the American Express Business Platinum card:

- Eight lounge visits at $35 USD (or $48 CAD) a visit

- A $200 travel credit

- Two hotel suite upgrades, one at $283, the other at $124

- A $200 delayed baggage claim from insurance which was paid out after your bags weren’t delivered on time coming home from a trip

Therefore, the total amount of value derived from the premium card at year’s end based on the full retail price would be $1,259. My choice to pay the annual fee would thus be based on whether I feel this was a good amount of dollars to get for an annual fee that’s potentially far north of $250.

Do you see now why banks would love to advertise such a valuation? While this number isn’t entirely inaccurate, it also doesn’t paint the full picture. I myself wouldn’t want to pay $283 to upgrade my room, nor would I wish to pay $48 every time I go into a mediocre Plaza Premium lounge.

This is how we arrive at the second baseline calculation method: that of assigning $0 in value to any and all benefits, then determining how much each individual benefit “costs” versus the annual fee of the card.

Valuing Your Premium Credit Card: Usage of Benefits

Let’s take a look at the second mechanism of calculating a baseline of value: one where each benefit has absolutely no monetary value.

The value is simply in using a benefit of any kind or not. The card I will dissect for this is the American Express Gold Rewards card, which comes with a $250 annual fee and a variety of features such as:

- $100 annual travel credit

- Four complimentary passes to Plaza Premium airport lounges

- 1 $50 USD NEXUS statement credit

- A $100 USD credit and room upgrade for select luxury hotel

- Hertz rental improvements, including vehicle upgrades

- A suite of insurance, including for travel

- Access to the Amex concierge

Therefore, if I wanted to maximize these and used both the travel and NEXUS credit, all four lounge passes, got upgraded by Hertz twice, booked one Hotel Collection hotel, and called the Concierge twice, then I would have used my benefits a total of 11 times. The $250 annual fee divided by 11 is $22.72.

By my final math, at year’s end, my lounge visits thus cost $22.72. My car rental upgrades cost $22.72. My $100 travel credit cost $22.72, calling the concierge has the same cost per call, and to quote the Slovenian philosopher Slavoj Zizek …”And so on and so on….”

My choice thus would be to determine if paying $250 for benefits that I value at $22.72 per use is worth it.

This method has its advantages, but again, it’s not necessarily one that I think most normal humans would attempt to replicate. For that, we have to go to my mixed method: a hybrid method of calculation.

Renewing Your Premium Credit Card: Hybrid Value Model

The previous two sections were for establishing a “baseline” of value: the first demonstrated the maximum value you might get, had you been willing to pay the full sticker price for things like lounge entries and suite upgrades.

A bank or issuer would love this math, because it allows them to in good conscience tell you that you get hundreds, if not thousands, of dollars of value out of their product.

The second method is for perennial cheapskates: people who want to know only how much each instance of using their benefits runs them, and thus they try to maximize uses to drive the cost per use down, then renew cards when that number is as minimized as they can manage.

However, what makes the most sense to me is to calculate the value based on two criteria: benefits that have a set monetary value, and benefits that you wouldn’t pay for.

I personally would never pay a dollar out of pocket for lounge access. Therefore, what matters most to me is finding out how much of my annual fee goes toward paying for lounge visits, and trying to keep that number low.

However, I do value other benefits such as travel insurance, hotel status, travel credits, and so on. That doesn’t mean I value them at their full stated retail price: instead, I assign some value to some benefits, and to others, I will discount off the face value based on what makes sense to me.

Is It Worth It To Renew My Premium Credit Card? – Examples

With the above information in mind, let’s take a look at a few examples of notable premium credit cards in both Canada and the United States to determine the value proposition of keeping these cards in your wallet year after year.

American Express Platinum Card

The American Express Platinum card is the most prominent premium credit card for Canadians, and easily one of the most talked about cards in the world of miles and points.

The American Express Platinum Card is a premium card offering a $200 travel credit and $200 dining credit. From access to participating airport lounges and special benefits at participating fine hotels around the world, to exclusive events and elevated service, experience the world with the many benefits of Platinum.

170,000 Membership Rewards points

$45,000

$3,400+

$799

Yes

Jul 28, 2026

Let’s start with analyzing the American Express Platinum card by looking at its annual fee: $799 per year. It also comes with a pile of benefits:

- An annual $200 travel credit

- An annual $200 restaurant credit (which must be redeemed in a single transaction of above $200 at a list of predetermined restaurants)

- Complimentary airport lounge access worldwide via the American Express Global Lounge Collection

- Complimentary Priority Pass

- Access to the American Express Platinum concierge

- Powerful travel insurance

- Marriott Bonvoy Gold status & Hilton Honors Gold status

- The occasional Amex Offer I actually find some value in (such as a discount or rebate on Marriott stays)

I’m showing you exactly how I would personally calculate the value I get from this card, and how I make my decision for myself. Your valuations may vary!

For this exercise, I will state that I hold the lounge access to have minimal monetary value: I would not pay the retail price of entry if I did not have this premium credit card. I also find the concierge to have no intrinsic value.

On the other hand, I value the $200 travel credit at its full face value. I discount the $200 restaurant credit to $150 because of the restrictions around its usage, and because I wouldn’t normally eat at such dining establishments. I feel the travel insurance has $100 in value annually, as this is what I’d pay for a travel insurance policy of similar quality.

Finally, there are the elevated hotel statuses. I don’t really value these highly, but I would be willing to pay $30 out of pocket for a hotel upgrade, so if I score a room upgrade from Hilton Gold (as I’m already a Marriott Titanium Elite member), I’ll consider that worth $30.

Therefore, my total monetary value from this card, assuming I get one suite upgrade in a calendar year, is $480 before lounge visits. Subtracted from the annual fee of $799, my lounge visits thus cost me $319.

On average, I visit lounges at least 16 times a year and never bother with the American Express Platinum Concierge service. I often include a second guest when entering lounges as I’m entitled to do so as part of the benefits. Let’s round 16 to 20 visits to account for guest entries. Thus, my lounge entries average about $16 ($319 divided by 20 visits), which is about $30 less per visit than the stated retail price.

I feel that these benefits combined provide me with enough value, and as a result, I will renew my American Express Platinum card again.

TD® Aeroplan® Visa Infinite Privilege Card

The TD® Aeroplan® Visa Infinite Privilege card is a popular card amongst Air Canada Aeroplan aficionados with higher personal or household incomes.

The TD® Aeroplan® Visa* Infinite Privilege* Card offers a variety of Air Canada benefits including priority boarding, free checked baggage, and Maple Leaf lounge access.

85,000 Aeroplan points

$24,000

$1,785+

$599

Yes

–

The TD Aeroplan Visa Infinite Privilege card takes the bank calculation approach in advertising the values of its ancillary services. This card has an annual fee of $599 and is an example of a product that requires you to know the terms, conditions, and features inside out to even get close to that much in annual value:

Let’s provide TD the benefit of the doubt on almost all their cost estimates, and accept that the $136 for NEXUS fees applies in the first year. This still makes it useless for the question of renewal, as you won’t be able to use the $136 again until your present NEXUS membership expires.

The savings on checked bags could likewise be significant… but only if you’re booking flights on Air Canada in economy class to make use of the free checked bag benefit. The maximum I could see occurring would be if you booked an Economy Basic fare to Europe for yourself and a travel companion, thus saving $75 per checked bag per direction:

As this is a niche redemption, we’ll take TD’s estimate of $140 in value. Let’s say the travel insurance package is also worth $100, and all the random Air Canada bonuses like priority boarding are worth $100 a year. So you’ve received $340 in value, meaning your effective annual fee is now $259.

But you still have a variety of lounge passes to use: 6 lounge passes via the Visa Companion app (ultimately they can be used for airport lounges in the DragonPass lounge program), and an unlimited amount of Maple Leaf Lounge visits within Canada. Let’s assume you use all six of the DragonPass lounge passes, and visit the Maple Leaf Lounge an additional 6 times for a total of 12 lounge visits. That means $259 divided by 12 visits = $21.50 a lounge visit.

This isn’t the worst value for lounge visits, but remember that the card comes with no travel credits or additional statuses. Moreover, the free checked bag benefit for the cardholder and up to eight guests on the same Air Canada itinerary only has value if you have booked an Air Canada fare class that doesn’t include complimentary baggage.

The TD Aeroplan Visa Infinite Privilege card is overall an underwhelming prospect for renewal under my calculation guidelines with my personal situation, but as always, do the math for yourself to determine what value you can expect to receive from this card year after year. It would also be worth reading our review of the TD Aeroplan Visa Infinite Privilege Card to make that decision for your own personal situation.

American Express Hilton Honors Aspire Card (US)

If the TD Aeroplan Visa Infinite Privilege might have less than optimal renewal potential, the case is completely reversed when we travel south of the border to the United States.

The premium credit card game in America is unparalleled due to the sheer level of competition, and each issuer is trying to outcompete the next in offering unique value that’s just hard enough to liquidate so as to keep you renewing your cards and paying those hefty annual fees.

An excellent example of this is the American Express Hilton Honors Aspire card (US), which charges an annual fee of $550 USD.

The American Express Hilton Honors Aspire Card offers up to a $200 semi-annual Hilton Resort credit, a quarterly $50 airline statement credit, instant Hilton Honors Diamond Elite status, an annual free night certificate, and more.

Check out our American Express Hilton Honors Aspire card review for more details.

150,000 Hilton Honors points

$6,000

$900+

$550

No

–

However, its benefits speak for themselves:

When we analyze these credits, we see that they are significantly easier to use, even if they may not have 100% of the listed value. For example, this $100 property credit that is also offered as a benefit on the Aspire card requires a cash booking at a luxury Hilton property at the full rack rate. It can be safely ignored, as the value just isn’t there.

On the other hand, the resort credits and flight credits can be easier to use than might meet the eye, especially if you intend on staying at or traveling to a lot of hotels within the Hilton Honors portfolio.

The annual Hilton Free Night Certificate itself is one of the most powerful in the entire hospitality industry and is worth several hundred dollars at least on its own, and can easily be worth north of $1,000 USD if used strategically. Lastly, Hilton Honors Diamond status, the highest tier of status in the loyalty program, is worth at least $500 USD just by rough approximation.

With $400 in credits, $500 in status, at least $300 in free night certificates, and $200 in flight credits you might only get $100 out of per year. These all easily outweigh the $550 USD fee, making this card a keeper if you also intend to stay at Hiltons as you’re getting at least $700-800 above the annual fee and that’s before factoring in things like credit card insurance.

In fact, it can even be worth it to hold multiple American Express Hilton Honors Aspire cards at the same time, to benefit even further.

Conclusion

Nobody likes paying annual fees, me least of all. However, premium credit cards can be worth it if they give you good value for the price that you pay to elevate your travel experiences, and if you can get over the mental roadblock of paying an annual fee.

Today we’ve explored a few methods we can use to precisely calculate just how much value you’re getting. Feel free to experiment or modify any of these methods to a system that works for you, as a great once told me that price is what you pay, but value is what you get. My goal has been to assist in helping to demystify what that value can be in cold, hard numbers.

Until next time, frugal fly with lounge stops.

Kirin Tsang

Latest posts by Kirin Tsang (see all)

- Canadian Credit Card Tiers: What They Mean - May 29, 2026

- Redeeming Virgin Atlantic Points in Europe: An Incredible Sweetspot - May 25, 2026

- Review: KLM Business Class (787-10) - May 20, 2026

- All of Hilton Honors Hotel Brands Explained - May 15, 2026

- American Express Acceptance in Canada: Better Than You Think - May 11, 2026

Super useful article – already sent it to a friend of mine!

Well done, Kirin. I like your new style of writing. Keep up the good work