Booking a flight entirely using points is what we live for here at Frugal Flyer. Whether it be Aeroplan points, WestJet points, British Airways Avios, or any Canadian bank loyalty programs, not paying for flights is a luxury of the credit card savvy.

The flip side is that credit cards are also the primary means that most of us use to insure our flights and trips against various risks – be it trip delay or cancellation, damaged baggage, or medical emergencies.

However, booking a flight with points adds a slight complication – many credit card insurance terms and conditions state that the entire cost of the trip must be charged to the card for the insurance to apply. How does this work when paying for the flight partially or entirely using points? Are you still covered?

In this article, we break down how travel insurance works on award flights and how you can best ensure that you’re insured!

How Does Credit Card Travel Insurance Actually Work?

When you travel outside your home province or country, it’s generally recommended to have travel insurance to protect you in the case of an emergency. Insurance coverage for travel generally falls under two categories:

- Travel medical insurance protects you in the case of a medical emergency or health complication, including hospitalization, medical evacuation, and so on. You are covered for a trip duration of up to a certain number of days and a certain amount, based on your age. Most credit card insurances don’t cover seniors, unfortunately.

- Trip protection insurance protects you in the case of various unexpected setbacks and logistical complications that can happen on a trip, including:

- Trip cancellation/interruption: if your trip is canceled due to unforeseen circumstances or you need to return home for an emergency, you can be reimbursed.

- Flight/trip delay: If your trip (generally the flight itself) is delayed for over a certain number of hours, you can be compensated.

- Lost, stolen, damaged, or delayed baggage: you can be compensated for replacing your baggage or essentials you’re missing in the case of a delay.

- Rental car collision, loss, and damage: you can be covered for a certain rental period up to a maximum retail price, with or without coverage for personal effects.

Credit card travel insurance is similar to other types of travel insurance offered by dedicated travel insurance agencies, but you are able to obtain coverage without an out-of-pocket cost.

Of course, like all insurance policies, the subtle differences in the amount, type of coverage, conditions of coverage, and so on, are often hidden in the fine print.

Most credit cards, especially the higher-end premium credit cards like World Elites and Visa Infinites, offer these travel insurances to the primary cardholder, and often dependents of the primary cardholder as well.

Emergency Medical Insurance: Flexible Eligibility

With emergency medical insurance, almost all credit cards that offer this coverage have no stipulation that you charge the trip to the card in order to be eligible. You qualify just for being a cardholder.

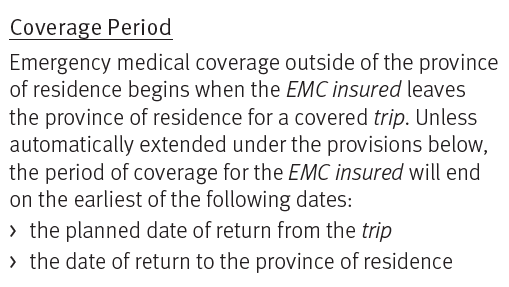

As long as you are leaving the province or country for travel, you will be eligible for coverage. For example, the wording in the insurance details for the National Bank World Elite Mastercard is as follows:

This means as soon as you leave the province for a covered trip, your coverage begins. There is no requirement at all for trip costs to be charged to the card. Simply hold the card open and you are eligible.

However, do be wary of specific exclusions and conditions. For example, if the trip duration is longer than the allowed coverage period, the entire trip will not be covered. There are usually exclusions for certain pre-existing medical conditions and if you partake in risky activities (like hang gliding for example). Some credit cards also require you to have public insurance in your home province to be covered by the credit card’s medical insurance policy.

So, although your credit card emergency medical insurance coverage is generally unaffected by booking using points, it’s another story when it comes to trip protection insurance.

Does Credit Card Trip Protection Insurance Apply on Flights Booked with Points?

The answer to this question is not straightforward: it depends on the specific card, type of insurance, and nature of the flight.

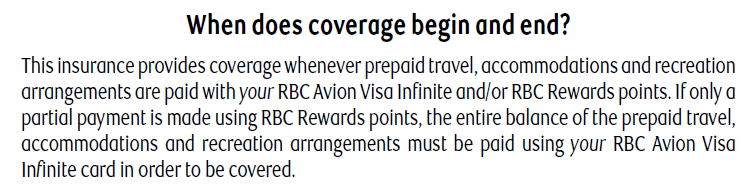

Many credit cards stipulate that for the coverage to apply, you must charge the entire trip cost to the credit card. For example, see the RBC Avion Visa Infinite coverage details for Trip Cancellation/Interruption insurance below.

Unless the entire trip cost is charged to the RBC Avion Visa Infinite, the coverage isn’t in effect. Note the exception for trips where RBC Avion Rewards points are used – this is a common theme amongst all the bank rewards programs, be it Amex Cards with Membership Rewards bookings, WestJet Mastercard with WestJet flights booked using WestJet points, Scotiabank cards with Scene+ travel bookings, and so on.

However, having to work around all these programs for a given trip is a bit of a hassle. Wouldn’t it be easier if a credit card offered insurance that covered award bookings made with points from any loyalty program? It turns out there are several cards in Canada that offer just that.

Which Credit Cards Cover Award Bookings with Any Loyalty Program?

There are a select few credit cards that flexibly cover all award bookings, regardless of which points program you use to book the award. These cards include the BMO Ascend World Elite Mastercard, the BMO CashBack World Elite Mastercard, and the National Bank World Elite Mastercard.

All of these cards generally offer coverage as long as there is at least a partial charge to the card. For example, if you book a flight with Aeroplan points, paying the taxes and fees with your National Bank World Elite Mastercard would make you eligible for the card’s travel insurance.

I would definitely recommend everyone hold at least one of these credit cards as a keeper card so that you always have a way to access travel insurance benefits when booking award flights. But which one should you choose?

See the table below for a handy comparison.

| BMO Ascend World Elite Mastercard | BMO CashBack World Elite Mastercard | National Bank World Elite Mastercard | |

|---|---|---|---|

| Rewards Program | BMO Rewards | Cash back | À la Carte Rewards |

| Annual Fee | $150 (FYF) | $120 (FYF) | $150 (FYF) |

| Emergency Medical | |||

| – Amount | $2,000,000 | $2,000,000 | $5,000,000 |

| – Coverage period | 21 days | 8 days | 60 days (<age 54) 31 days (55 to 64) 15 days (65 to 74) |

| – Maximum age | Age 64 and under | Age 64 and under | Age 76 and under |

| Trip Cancellation or Delay (before departure) | |||

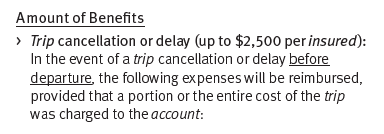

| – Maximum coverage | $2,500 per insured (up to $5,000 per account) | None | $2,500 per insured |

| – Minimum flight delay time | N/A – cancelation only | None | 4 hours |

| – Allowable subsistence expenses | N/A – cancelation only | None | $250 per day (up to $500 total) per insured |

| Trip Interruption (after departure) | |||

| – Maximum coverage | Lesser of $2,000 per insured person or the partial amount charged to the card | None | $5,000 per insured |

| – Minimum flight delay time | N/A | None | 6 hours |

| – Allowable subsistence expenses | $150 per day per insured person | None | $250 per day (up to $3,000 total) per insured |

| Flight Delay Insurance | Up to $500 per account (minimum 6-hour delay) | Up to $500 per account (minimum 6-hour delay) | Up to $500 per person (minimum 4-hour delay) |

| Lost, Stolen, or Damaged Baggage | Up to $750 per insured person ($2,000 per account) | Up to $750 per insured person ($2,000 per account) | Up to $1,000 per insured person |

| Delayed Baggage | Up to $200 for 12-hour delay or more | Up to $200 for 12-hour delay or more | Up to $500 for 6-hour delay or more |

| Rental Car Collision Loss & Damage Insurance | |||

| – Maximum rental period | 48 days | 48 days | 48 days |

| – Maximum retail price | $65,000 | $65,000 | $65,000 |

| – Personal effects coverage | $1,000 per person ($2,000 per rental period) | $1,000 per person ($2,000 per rental period) | None |

As you can see from the chart, the National Bank World Elite Mastercard edges out the competition in most categories of travel insurance, including a vastly superior medical insurance amount of 5MM, with a longer trip duration and a wider age range. This makes the National Bank World Elite Mastercard my choice for travel insurance.

There is also a bit more leeway in minimum trip delay time (4 hours vs. 6 hours for flights, 6 hours vs. 12 hours for baggage, etc.). Rental car insurance is comparable, although the National Bank doesn’t cover personal effects from theft.

The National Bank World Elite Mastercard offers benefits that include an annual $150 travel credit and access to the National Bank VIP airport lounge in the Montreal Airport International terminal.

Earn when you apply through Frugal Flyer.

35,000 À la carte Rewards

$20,000

$500+

$150

Yes

Jun 29, 2026

It’s also important to mention that with baggage delay, the National Bank World Elite coverage won’t apply if the full cost of the flight wasn’t charged to the card.

If you decide to sign up for the National Bank World Elite Mastercard, don’t forget to apply via the FlyerFunds Rebate program to get some additional cash for getting approved!

Which Credit Cards Should I Use When Booking with Aeroplan Points?

While I don’t recommend chasing every credit card with every program to maximize insurance coverage, Aeroplan is Canada’s premier points program and it’s worth mentioning that Aeroplan co-branded credit cards also extend travel insurance benefits to trips booked using Aeroplan points. Just remember to charge the taxes and fees to the card.

Aeroplan has co-branded cards with Amex, TD, and CIBC, included in the below table.

| Credit Card | ||

|---|---|---|

|

150,000 Aeroplan points Estimated value: $3,150 Ends Jul 28, 2026 |

|

|

75,000 Aeroplan points Estimated value: $1,575 |

|

|

75,000 Aeroplan points Estimated value: $1,575 |

|

|

100,000 Aeroplan points Estimated value: $2,100 |

|

|

90,000 Aeroplan points Estimated value: $1,890 |

|

|

85,000 Aeroplan points Estimated value: $1,785 |

|

|

60,000 Aeroplan points Estimated value: $1,260 |

|

|

50,000 Aeroplan points Estimated value: $1,050 |

|

|

40,000 Aeroplan points Estimated value: $840 |

|

|

45,000 Aeroplan points Estimated value: $945 |

|

|

20,000 Aeroplan points Estimated value: $420 |

|

|

10,000 Aeroplan points Estimated value: $210 |

|

If you already hold and use one of these cards and are an avid Aeroplan flyer, you can safely pay for your award bookings with these cards and rest easy knowing you’re covered by the credit card insurance benefits.

Conclusion

Travel insurance is something you never plan to use. But in worst-case scenarios, it can be incredibly helpful to have. As a savvy credit card holder, you can benefit from the travel insurance provided by your credit card. However, you need to be especially careful when booking a trip using points. Read the fine print carefully on your credit card to make sure your coverage applies, and if not, you should consider adding one of the cards mentioned in this article to your wallet.

Reed Sutton

Latest posts by Reed Sutton (see all)

- byAir: The Ultimate Flight Tracker App? - Jun 12, 2026

- Review: TAP Air Portugal Business Class (A330-900neo) - Jun 3, 2026

- Earn Cash Back Rebates on RBC Bank Accounts - Jun 2, 2026

- BMO VIPorter World Elite: Earn 70,000 VIPorter Points & $200 FlyerFunds - May 16, 2026

- Edmonton Miles & Pints Meetup (June 2026) - May 12, 2026

Hello, I booked international flights using Airmiles reward miles. I paid taxes and fees with another credit card (best travel insurance – but now may have unduly created a bad situation). After many, many calls with Airmiles, BMO and the third party insurer for Airmiles, I still haven’t got a straight answer about Airmiles reward miles coverage. One agent told me I was automatically covered, another that I had to add a specific component of coverage to my Mastercard, and another, the third party insurer is the only reward mile protection).

I used my AM reward miles to book the flights, but charged it to another credit card (not the BMO World Elite Mastercard).

Will I have reward mile coverage automatically as a BMO world elite mastercard holder?

Do I need to buy third party insurance to protect my reward miles? Thanks in advance for any concrete answers you can provide!

What specific insurance coverage are you referring to? There isn’t really any way to cover your miles themselves with insurance, our article is more about being covered for other types of travel insurance such as flight delay/cancellation or medical travel insurance, in the case where you’ve used award miles to pay for the flights. So you wouldn’t likely get your miles back in any case of mishap, but may be able to be compensated if you had to rebook a flight to get home due to a cancellation, for example.

If you used a credit card that doesn’t explicitly state that it covers travel paid with only partially by the credit card, then you would not be covered. You will need to look in your card’s certificate of insurance for this verbiage. This is all explained clearly in the above article.

Thank you for your speedy reply. I was indeed looking for any information on protecting the reward miles used specifically, through a travel-related credit card. Having booked four flights, I was hoping to find some protection if we needed to cancel. I appreciate your response.

Thank you for the article, very interesting, however I have a question, which I haven’t found answer to anywhere so far. I bought an all-inclusive trip last year with Sunwing, paid with my BMO WE full price, however due to covid situation last December had to cancel the trip. Sunwing provided their own voucher in lieu of the sum of the trip paid. I used the voucher this year to pay for a similar trip later this month. Will the BMO WE cover this trip due to the fact, that the initial trip purchase was maid to the card, despite the fact, that this time I used the company supplied voucher given in lieu of the payment? Thank you.

Most likely it would not be covered, but the only way to know for sure would be to call BMO.

Is there any way to use part of the voucher and cover some portion of the trip/taxes/fees with your BMO card instead? This would guarantee coverage.

How do you interpret “Charge at least 75% of the full ticket cost” and “Charge the full cost of your airplane, train, bus or cruise ship tickets to your Card” when redeeming Aeroplan points but charges taxes amount on the card? Would there still be coverage?

No there wouldn’t likely be coverage. If you’ve got an award flight paid primarily with points, you are looking for the verbiage “partial cost” on the insurance description.

Hello, thank you so much for this article. I bought my Qsuite with my Avios and paid the taxes with my BNC WE. From Dubai to Montreal I’m on 2 separate reservation numbers with a 2 hours delay in Doha. Historically, that flight from Dubai to Doha is never delaid, but what if it is on the day I leave Dubai and I miss my flight in Doha? What will be my insurance coverage from my BNC WE? Will they reimburse only the taxes or the Avios as well? Will I be rescheduled in another Qsuite at the insurance cost?

Hi Lucy,

This is a bit of a unique situation – travel insurance will not cover if you miss a flight due to being booked on a separate itinerary. You would be protected if both flights were on the same itinerary, and thus, the carrier would have an obligation to get you to your final destination if you missed your second flight as a result of a delay.

There are risks when it comes to positioning with two different itineraries; 2 hours would be a tight gap that I would be concerned about making.

Thank you for your response, I’m back in Canada and everything went well. In the insurance booklet under trip cancellation, i think my situation would have been covered. I will avoid booking 2 flights in different reservation number in the future, but I’m wondering how the insurance with BNC WE works when we reserve with points. What will they reimbursed if the cancellation situation is accepted?

https://www.nbc.ca/content/dam/bnc/particuliers/pdf/assurance/certificate-713705-3.pdf

« a departing, connecting or return flight for the trip

that he missed as a result of a mechanical failure

of the means of transportation, weather conditions,

a road accident, police-directed road closure or change of schedule by the common carrier (bus, train, etc.), provided that the original travel arrangements

would have allowed him to arrive at least 2 hours

before the flight »

It does look like if there is a gap of 2 hours, you’d be eligible. However, you would not get reimbursed points, only what is charged to the account.

“The unused and non-refundable portion of prepaid travel arrangements for the insured’s trip charged to the account,”

You would be able to get reimbursed for hotel cost or cost for alternative travel expenses (eg. a rebooked flight in the lowest-cost economy class).

These details are in the table on the page after the text you quoted.

Regards,

Reed